Fintech Lending in India: How Businesses Are Getting Loans in Days

Understand fintech lending for Indian startups and SMEs: how it works, benefits, risks, and how to judge if it fits your business financing needs.

Growth often strains cash flow. A business may have steady orders but still feel squeezed when receivables are delayed, inventory needs funding, or repayments are poorly timed. This is a common issue for Indian startups and SMEs, with 2.07 lakh recognized startups and small-business commercial credit exposure reaching ₹35 lakh crore by March 2025.

Fintech lending platforms stand out because they deliver speed, clarify checks, and offer loan structures businesses can assess against actual cash flow, eligibility, and document readiness.

This blog explains fintech lending, shows how it works, highlights where it differs from traditional business lending, and outlines what to review before applying.

Key Takeaways

- Fintech lending is transforming business finance: It replaces slow, paperwork-heavy bank processes with fast, digital, and data-driven loan approvals.

- Access to credit is expanding for SMEs: Alternative data like GST filings, bank transactions, and cash flow patterns enable funding for businesses traditionally excluded from formal lending.

- Speed and efficiency are major advantages: Loan approvals and disbursals can happen within days, helping businesses manage liquidity and act on growth opportunities faster.

- Flexible financing aligns with real cash flows: Models like revenue-based financing, invoice discounting, and supply chain finance are designed to match how businesses actually earn and spend.

- Choosing the right platform matters: With marketplaces like Recur Club, businesses can access multiple lenders, compare structures, and secure tailored financing with faster disbursal timelines.

What Is Fintech Lending, and Why Does It Matter?

Fintech lending refers to the use of digital technology, alternative data, and automated credit models to assess creditworthiness and provide loans faster than traditional financial institutions.

Instead of relying only on credit scores, collateral, and historical financial statements, fintech lenders evaluate real-time business signals such as:

- GST filings

- Bank transaction data

- Cash flow patterns

- Recurring revenues

This data-driven approach allows lenders to make faster, more accurate decisions, often within days instead of weeks.

Why Fintech Lending Matters for Indian Startups in 2026

- Quick Access to Working Capital

Traditional banks are slow and often require excessive paperwork. In contrast, fintech lenders offer fast, flexible loans that help businesses manage cash flow gaps in real time, ensuring smooth operations. - Credit for Underserved Businesses

Furthermore, many startups lack a credit history, making them ineligible for traditional loans. Fintech platforms use alternative data, such as bank transactions and GST filings, to assess risk and offer funding to businesses that banks overlook. - Loans that Match Startup Cycles

Additionally, unlike traditional lenders, fintech lenders offer products like invoice financing and lines of credit that align with startups' irregular cash flow and seasonal nature, enabling faster growth and smoother scaling. - Digital and Accessible

Moreover, fintech lending is fully digital, providing easy access to capital for businesses in rural or underserved areas, thereby reducing geographic and demographic barriers to credit. - Lower Costs and More Transparency

Finally, by automating processes, fintech platforms reduce operational costs and offer lower rates with clear, transparent terms, unlike the hidden fees often associated with traditional bank loans.

Recur Club helps Indian businesses do exactly this, access 150+ lenders, 15+ debt structures, and expert capital advisory through a single platform, with disbursals in as little as 72 hours.

Also Read: The Rise of Fintech Alternative Lending: Benefits for SMEs

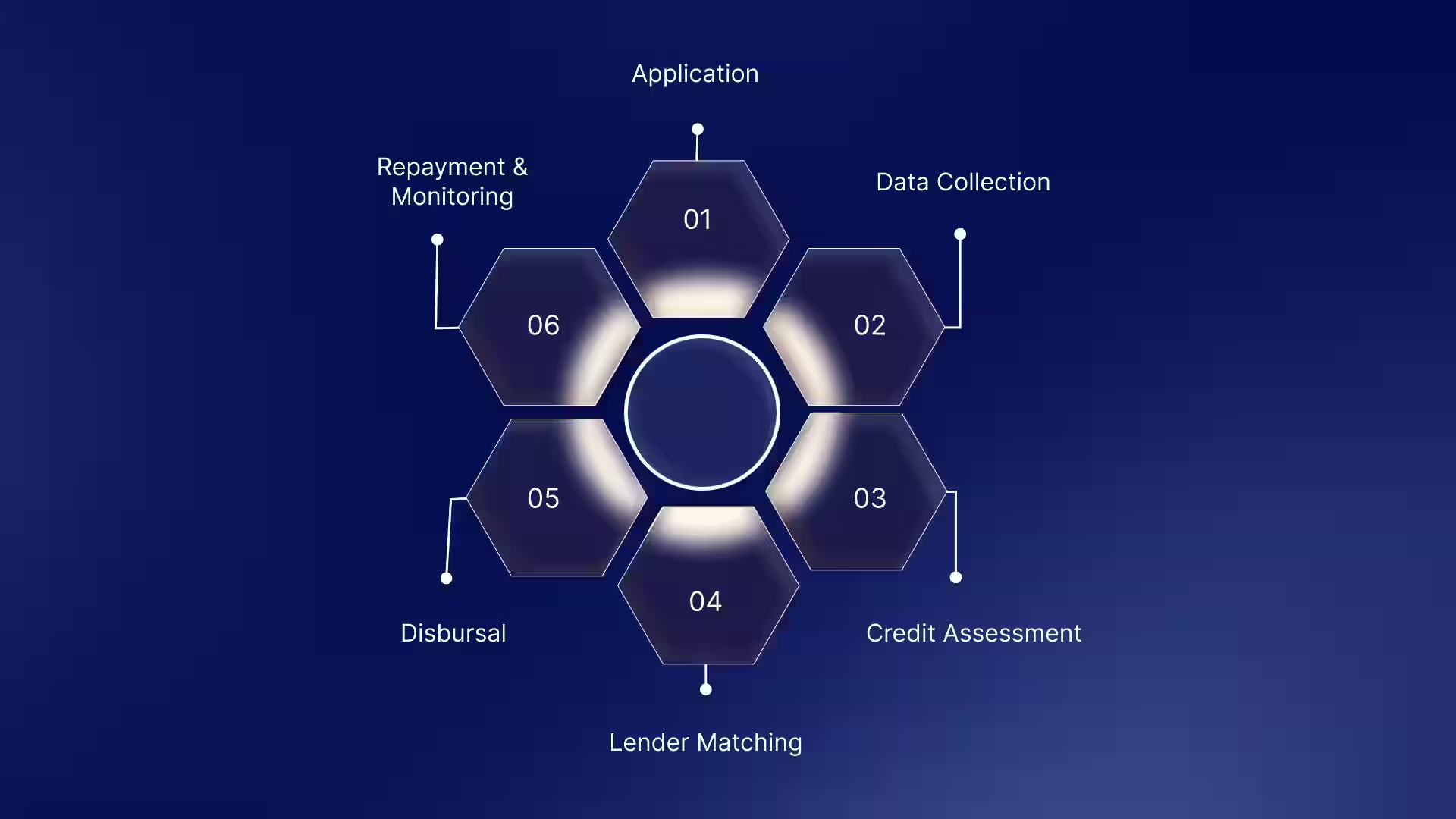

How Fintech Lending Works: Step-by-Step Process Explained

Here’s how most fintech lending platforms operate end-to-end:

1. Application

The process starts with a single digital application.

Businesses submit basic details such as:

- Company profile

- GST number

- Bank account information

- Financial statements (if available)

Unlike traditional banks, there’s no need for branch visits or extensive paperwork; everything is initiated online.

2. Data Collection

Once the application is submitted, the platform securely retrieves structured financial data through integrations and consent-based access.

Key data sources include:

- GST filings: Provide insights into revenue trends and tax compliance

- Bank statements: Help analyse cash flow patterns, including inflows and outflows

- MCA filings: Offer details on company financials and director information

- Recurring revenue data: Highlight subscription-based or predictable income streams

Together, these inputs create a real-time financial profile of the business that is significantly more comprehensive than traditional static balance sheets.

3. Credit Assessment (AI/ML Underwriting)

Instead of manual credit checks, platforms use AI and machine learning models to evaluate:

- Revenue consistency and growth

- Cash flow stability

- Expense behavior

- Existing liabilities and repayment patterns

These models analyse hundreds of data points simultaneously, identifying patterns that traditional underwriting may miss.

4. Lender Matching

For marketplace-led fintechs, the next step is matching the business with the right lenders.

Instead of applying to multiple institutions separately:

- The platform evaluates eligibility across its lender network

- Businesses receive multiple loan offers

- Different structures are presented (working capital, invoice financing, revenue-based loans, etc.)

This increases both approval probability and access to better-fit financing options.

5. Disbursal

Once the borrower selects an offer, the remaining steps are completed quickly and digitally.

- Documentation: Completed online with minimal paperwork

- Disbursement: Funds are credited directly to the business account

Typical timelines:

- Simple products: 24 to 72 hours

- Complex structures: A few days to a few weeks

The entire process eliminates physical bottlenecks and reduces dependency on multi-layer approvals, making fund access significantly faster.

6. Repayment & Monitoring

Repayment is designed to align with business cash flows.

Common structures include:

- Fixed EMIs

- Revenue-linked repayments

- Automated deductions from bank accounts

At the same time, fintech platforms continuously monitor cash flow health and repayment behaviour. This enables dynamic risk management, along with opportunities for top-up financing or restructuring.

Fintech lending runs on more than capital, it runs on intelligence. That’s where AICATech by Recur Club takes the lead. It’s an AI-native lending platform that powers faster, smarter, and more transparent credit decisions for lenders and fintechs alike.

If you’re looking for funding that keeps pace with your business, this kind of infrastructure matters.

How Fintech Lending Differs from Traditional Bank Lending

While both fintech platforms and banks provide capital, the way they operate is fundamentally different:

Speed & Process

Traditional banks rely on manual underwriting, physical documentation, and multiple approval layers. Fintech platforms automate this entire journey, enabling quicker approvals and faster disbursals.

Data & Risk Assessment

Banks primarily evaluate past financials, credit scores, and collateral. Fintech lenders go deeper, using real-time operational data to assess a business’s actual performance and repayment capacity.

Accessibility

Bank loans often exclude early-stage businesses or those without strong credit history. Fintech lending expands access by supporting startups and SMEs that may not meet traditional eligibility criteria.

Flexibility

Traditional loans come with rigid structures and repayment schedules. Fintech models offer more flexible products, like revenue-based financing or invoice discounting, aligned with business cash flows.

Take Wellversed, a health and wellness startup, for example. They needed capital for expansion but were facing long delays with traditional funding options. Partnering with Recur Club, they completed due diligence in just 4 days and raised the necessary debt capital. This quick access to funding helped them increase revenue by 117% and EBITDA by 63%, all while maintaining ownership control.

So, if you're still waiting weeks for loan approval, you don’t have to. Recur Club offers flexible financing models that can help you secure capital in days, not months.

Also Read: Top Lending Fintech Companies in India: What You Need to Know

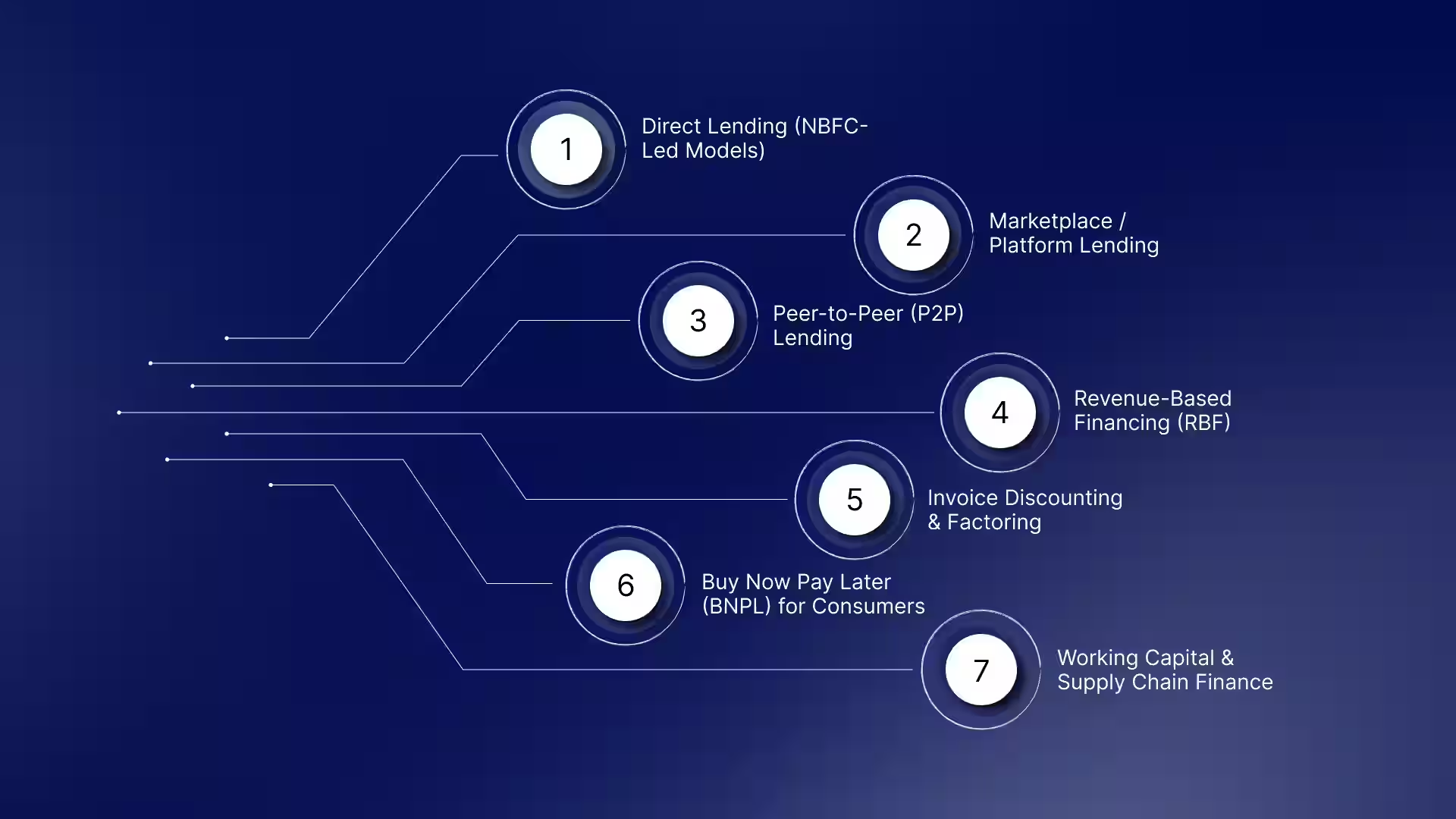

Types of Fintech Lending Models

Fintech lending is not a single product—it’s an ecosystem of different models designed to serve specific borrower needs, risk profiles, and business stages. Understanding these models helps businesses choose the right financing structure, not just the fastest one.

1. Direct Lending (NBFC-Led Models)

In this model, fintech companies lend directly from their own balance sheet, typically operating as or in partnership with NBFCs.

- The fintech controls underwriting, pricing, and disbursal

- Faster approvals due to in-house decisioning

- Common for small business loans, personal loans, and credit lines

Best for: Businesses looking for quick, standardised loan products.

2. Marketplace / Platform Lending

These platforms act as aggregators or intermediaries, connecting borrowers with multiple lenders.

- Single application that gets you matched with multiple banks/NBFCs

- Compare different loan offers and structures

- Often includes advisory-led structuring

Recur Club also focuses on aligning financing options with a business’s cash flow patterns and growth stage, making the selection process more strategic than purely transactional.

Best for: Businesses seeking better rates, higher approval chances, and customised debt structures.

3. Peer-to-Peer (P2P) Lending

P2P platforms connect individual lenders with borrowers, removing traditional financial institutions from the equation.

- Platform facilitates matchmaking and compliance

- Investors earn returns; borrowers get access to alternative capital

- Typically regulated with caps and restrictions in India

Best for: Small borrowers or early-stage businesses with limited access to institutional credit.

4. Revenue-Based Financing (RBF)

A modern model where repayment is linked to future revenue performance.

- No fixed EMI; repayments are a % of monthly revenue

- No equity dilution

- Works best with predictable income streams

Best for: SaaS, D2C, and subscription-driven businesses.

5. Invoice Discounting & Factoring

This model unlocks cash tied up in unpaid invoices.

- Businesses sell invoices to lenders at a discount

- Immediate liquidity without waiting for customer payments

- Factoring may also include collections support

Best for: Businesses with long receivable cycles or B2B operations.

6. Buy Now Pay Later (BNPL) for Consumers

BNPL enables consumers to purchase now and pay later in instalments.

- Widely embedded in e-commerce and checkout flows

- Drives consumer demand, indirectly benefiting merchants

- Typically short-term, small-ticket financing

Best for: Consumer purchases (but relevant for businesses via increased sales conversion)

7. Working Capital & Supply Chain Finance

These solutions address day-to-day operational funding needs.

- Includes credit lines, vendor financing, and purchase order financing

- Often linked to supply chain relationships and transaction data

- Helps maintain liquidity without long-term debt commitments

Best for: Businesses managing inventory, vendor payments, or seasonal demand

How SMEs and Startups Can Strengthen Their Fintech Lending Application

A strong fintech lending application is not just about speed. It is about presenting clear, consistent, and reliable financial data that aligns with how lenders assess risk.

Since most fintech lenders rely on automated underwriting and real-time data, even small gaps in your financials can affect approval timelines, loan terms, or eligibility.

What Lenders Look For

- Consistent revenue over the last 6 to 12 months

- Clean and traceable cash flow through bank statements

- Timely GST and statutory compliance

- Clear visibility of existing debt and obligations

- Accurate and matching data across all documents

Fintech Lending Application Checklist

|

Checklist Item |

What You Should Ensure |

Why Lenders Need It |

|

GST Filings |

Filed regularly with no gaps |

Confirms revenue trends and compliance |

|

Bank Statements (6–12 months) |

Stable inflows and controlled expenses |

Assesses cash flow and repayment ability |

|

Revenue Consistency |

Predictable monthly performance |

Reduces perceived risk |

|

Existing Debt Summary |

All loans and EMIs clearly listed |

Evaluates leverage and repayment burden |

|

MCA Filings / Financials |

Updated and accurate |

Validates business credibility |

|

Invoice Records |

Clear receivables and timelines |

Supports invoice-based financing decisions |

|

Unit Economics |

Positive or improving margins |

Indicates business sustainability |

|

Liquidity / Runway |

At least 3–6 months of runway |

Reduces short-term default risk |

|

KYC Documents |

Complete and consistent |

Speeds up verification |

|

Business Profile |

Clear model and growth plan |

Helps contextual credit assessment |

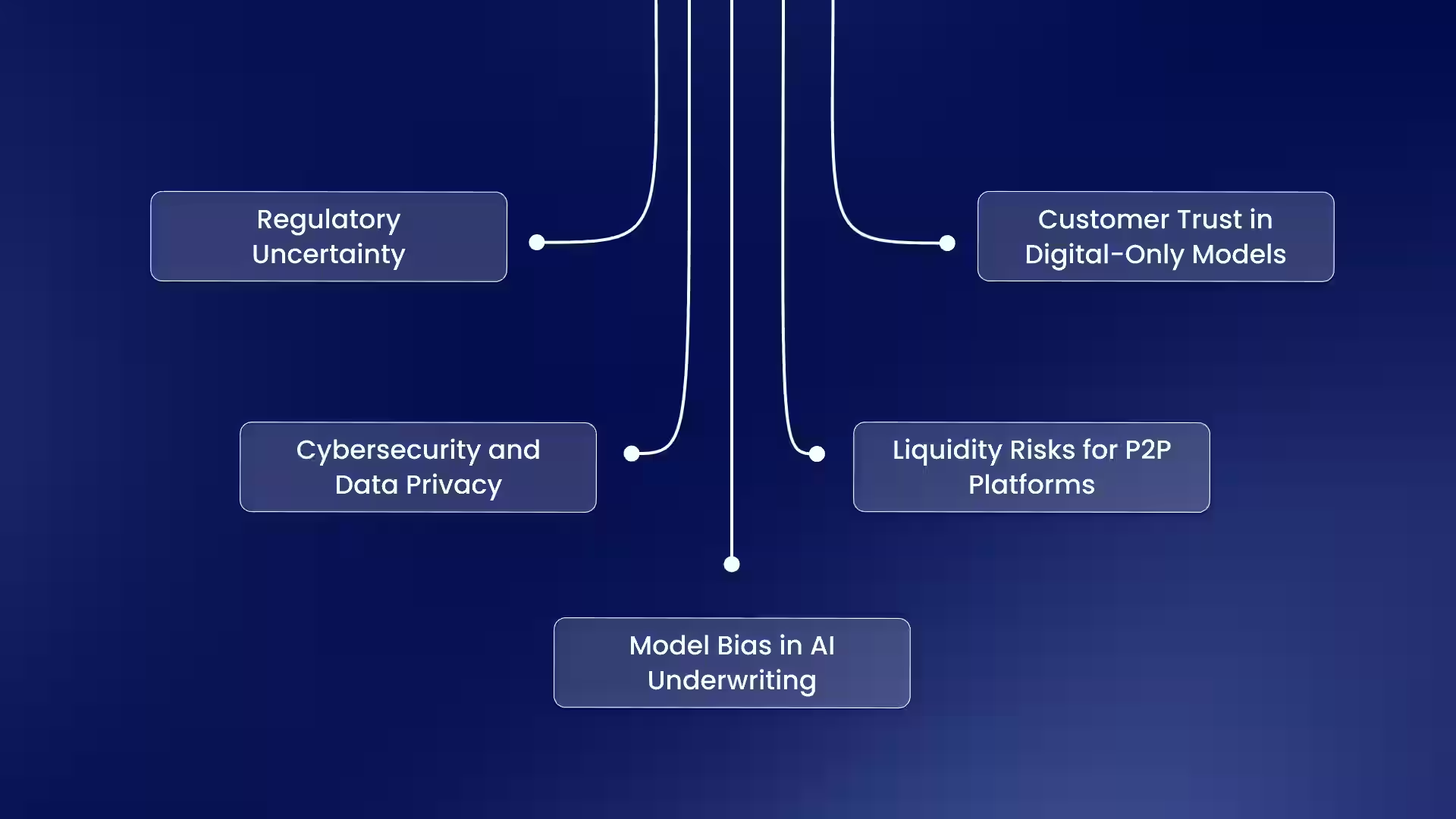

Challenges and Risks in Fintech Lending

While fintech lending has unlocked speed and access, it also introduces new layers of risk that both platforms and borrowers must navigate carefully.

1. Regulatory Uncertainty

- Regulations around digital lending and data usage continue to evolve

- Platforms must align with guidelines from the Reserve Bank of India

- Policy changes can quickly impact business models and scalability

2. Cybersecurity and Data Privacy

- Heavy reliance on sensitive financial data increases cyber risk

- Data breaches can cause financial and reputational damage

- Compliance with laws like the DPDP Act adds complexity

3. Model Bias in AI Underwriting

- AI models can reflect biased or incomplete data

- New or informal businesses may be misclassified as high-risk

- Lack of transparency raises fairness concerns

4. Liquidity Risks for P2P Platforms

- Dependence on investors makes capital supply volatile

- Economic downturns can reduce funding availability

- Limited balance sheet backing affects stability

5. Customer Trust in Digital-Only Models

- Lack of physical interaction can reduce borrower trust

- Concerns around hidden charges and data misuse persist

- Trust depends on transparency, support, and user experience

Recur Club’s Approach: Advisory + Marketplace

Unlike NBFC lenders that issue loans off their own balance sheet, Recur Club is a smart debt marketplace. We combine technology-driven underwriting with expert capital advisory, enabling companies to:

- Access 150+ lenders through a single process.

- Explore 15+ debt structures from working capital lines to structured NCDs.

- Get tailored guidance on the right debt mix for growth.

- Achieve disbursals within just 72 hours for straightforward structures.

Real-World Impact:

- Primebook: Raised ₹1 Cr in revenue-based financing via Recur Club to scale affordable laptops after its Shark Tank India appearance.

- CollegeDekho: Secured ₹40 Cr through structured debt, enabling expansion ahead of peak admissions.

With over ₹2,500 crore disbursed to startups and mid-market companies, Recur Club proves that fintech lending goes beyond transactional loans, offering strategic financing with expert advisory support.

Conclusion

Fintech lending is reshaping how Indian businesses access growth capital. By combining speed, data-driven decision-making, and flexible financing structures, it addresses long-standing gaps in traditional lending.

For founders and finance leaders, the shift is not just about faster approvals; it’s about aligning capital with real business performance. Whether it’s managing working capital, unlocking cash from receivables, or funding expansion, fintech models offer solutions that adapt to how businesses actually operate.

As digital infrastructure and regulatory clarity continue to evolve, fintech lending is set to play an even larger role in enabling sustainable, scalable growth for startups and SMEs across India.

Frequently Asked Questions

1. What types of fintech business loans does Recur Club offer?

Recur Club connects businesses with multiple lenders, offering access to over 15+ credit structures. These loans are facilitated through Recur Club's network of 150+ institutional lenders.

2. How quickly can I receive loan approval and funds from Recur Club?

Most businesses can expect loan approval and fund disbursement within 72 hours for certain products (like working capital loans and invoice discounting). However, larger, more complex loan structures like structured debt may take longer.

3. What are the eligibility criteria for obtaining a fintech loan on Recur Club?

To qualify, your business should be operational for at least 3 months, have a minimum annual revenue of ₹10 lakhs, and maintain sufficient liquidity (3 months of runway). Recur Club also considers alternative credit data to help businesses with limited traditional credit histories access capital.

4. How transparent are the loan terms and interest rates at Recur Club?

Yes, Recur Club guarantees full transparency in terms of pricing and fees. All interest rates, processing fees, and repayment schedules are outlined upfront.

5. Does Recur Club offer expert support for fintech loan applications and repayments?

Yes, Recur Club offers advisory services through dedicated capital advisors who guide you through the entire loan process. This includes helping you select the most suitable loan product from the available lenders and providing support throughout the repayment phase.

6. Is fintech lending safe for small businesses in India?

Yes, fintech lending is generally safe for small businesses, provided you borrow from platforms that are RBI-regulated or operate in partnership with licensed NBFCs. Look for lenders that are transparent about fees, follow data protection guidelines under the DPDP Act, and clearly disclose repayment terms upfront. As with any financial product, always read the loan agreement carefully before signing.

7. What is the difference between fintech lending and NBFC lending?

NBFCs (Non-Banking Financial Companies) are regulated institutions that lend from their own balance sheet. Fintech lending platforms may operate as NBFCs themselves, or they may function as marketplaces that connect borrowers with multiple NBFCs and banks. The key difference is that fintech platforms typically offer faster processing, digital-first experiences, and access to multiple lenders through a single application, whereas a standalone NBFC offers only its own loan products.

8. Can a startup with no credit history get a fintech loan in India?

Yes. Unlike traditional banks that rely heavily on credit scores and collateral, many fintech lenders use alternative data, such as GST filings, bank transaction history, and recurring revenues, to assess creditworthiness. This makes fintech lending especially valuable for early-stage startups or businesses that are new to formal credit. Some platforms, like Recur Club, require as little as 3 months of operations and ₹10 lakhs in annual revenue to qualify.

9. What documents are typically required for a fintech business loan?

Most fintech platforms keep documentation minimal compared to traditional banks. Commonly required documents include GST registration and filings, bank statements (typically 6–12 months), MCA or company incorporation documents, PAN and KYC details of directors, and basic financial statements. For certain products like invoice discounting, you may also need to share outstanding invoices or purchase orders.

10. How is repayment structured in fintech lending?

Repayment structures in fintech lending vary based on the loan product. Term loans typically follow fixed monthly EMIs, while revenue-based financing links repayments to a percentage of your monthly revenue, making it more flexible during slower months. Invoice discounting is usually repaid once your customer settles the invoice. Many platforms also support automated bank deductions to simplify the repayment process and reduce the risk of missed payments.

Related Articles

Proforma Invoice Financing: How Businesses Fund Orders Before Billing

Proforma invoice financing helps fund orders before billing. Learn uses, format, examples, and how businesses manage upfront costs effectively.

Debt Financing Agreements for Indian Startups: Key Terms and Negotiation Tips

What is a debt financing agreement? A practical guide for Indian startups covering covenants, repayment terms, defaults, and risks.

Financial Forecasting for Startups: Build Projections That Help You Raise Capital

Master financial forecasting for startups with revenue, expense, and cash flow projections to plan growth and attract investors.

Talk to our experts and find the right financing solution.

Talk to Our Experts →