Permanent Working Capital: Meaning and How to Finance It Smartly

Understand permanent working capital, how much you need, and the smartest ways to finance it without cash flow stress.

Profit is not the problem. Timing is. Salaries go out on the 1st, vendors expect consistency, and rent does not wait for your receivables to clear. Customer payments stretch to 60–90 days, tax credits get delayed, and one mismatch triggers a chain reaction. Founders are told to "manage cash flow better," but that advice ignores a harder truth: some expenses are fixed, unavoidable, and constant.

Recent reports estimate that over ₹7.3 lakh crore remains locked in delayed receivables at any given time in India, quietly choking liquidity across businesses. The issue is not revenue volatility. It is the absence of a baseline capital buffer that protects operations when inflows lag behind outflows.

This is where permanent working capital becomes critical, the minimum cash your business must always maintain to run without disruption, regardless of monthly fluctuations. In this article, you will learn what it means, how to calculate it, and how to fund it in a way that aligns with predictable expenses, so you can avoid repeated short-term borrowing and maintain operational stability with clarity.

Key Takeaways

A permanent working capital loan helps businesses fund their baseline operating expenses consistently, preventing cash flow gaps caused by delayed receivables.

Permanent working capital is the minimum cash required to run daily operations, covering fixed costs like salaries, rent, and inventory, regardless of revenue timing.

It can be estimated using current assets minus current liabilities, with requirements influenced by sales cycles, payment delays, and growth pace.

Without a stable capital buffer, businesses risk cash flow mismatches, leading to operational disruptions and repeated short-term borrowing.

Long-term or structured financing options such as term loans or revenue-based financing, are better suited than short-term credit for funding permanent needs.

Recur Club is an AI-native debt platform and marketplace that helps businesses access non-dilutive capital aligned with predictable expenses, improving cash flow stability without rigid repayment pressure.

What is Permanent Working Capital?

Permanent working capital is the minimum cash your business must always have on hand to run day-to-day operations. This amount stays relatively steady over time and doesn’t depend on monthly revenue swings.

It typically covers:

Salaries and vendor payments

Rent, utilities, software tools, and basic overhead

Core inventory or production inputs

Examples that founders experience daily:

Payroll continues even when large invoices are still in the 60–90 day cycle.

Inventory or raw materials must be purchased before customer payments arrive.

For SMEs and recurring-revenue businesses, keeping this baseline funded prevents cash gaps, avoids emergency credit, and maintains operational predictability.

Also Read: Sources of Working Capital: How SMEs Can Fund Daily Operations.

Calculating and Managing Permanent Working Capital

Calculating permanent working capital helps determine the baseline funds a business must maintain at all times. The simplest way to estimate it is:

Formula: Permanent Working Capital = Current Assets – Current Liabilities

This calculation shows how much liquidity remains after meeting short-term obligations. A consistent positive balance indicates that a company can sustain its daily operations without additional borrowing.

Key factors that influence the required level include:

Sales cycle: Longer sales or production cycles increase the need for steady capital.

Customer payment terms: Extended credit periods can delay inflows and tighten cash flow.

Business growth rate: Expanding operations or new product lines raise the baseline working capital requirement.

Several conditions make managing permanent working capital more complex. Many SMEs face delays in customer payments, often extending beyond 60–90 days. GST refunds and compliance procedures can also temporarily block cash. Additionally, supply chain disruptions, such as delayed shipments or rising input costs, add pressure to maintain sufficient liquidity.

Practical steps for better management:

Monitor cash flow weekly, not monthly.

Automate invoicing and follow-ups to reduce payment delays.

Build a reserve for tax or compliance-related hold-ups.

Review supplier credit terms regularly.

Also, Check: Understanding Collateral-Free Loans: Meaning and How They Work.

Why Permanent Working Capital Matters for Businesses

Revenue may fluctuate, but expenses do not wait. Permanent working capital ensures your business can operate smoothly without scrambling for funds every month.

Ensures Operational Continuity

Every business has non-negotiable expenses that must be paid regardless of sales performance.

Salaries, rent, and utilities continue even in slow cycles.

Minimum inventory must be maintained to fulfil orders.

Vendor payments need consistency to retain supplier relationships.

Without a clearly defined level of permanent working capital, businesses face frequent cash flow gaps and operational disruptions. Maintaining it builds credibility with employees, vendors, and customers while reducing dependency on last-minute, high-cost borrowing.

Prevents Cash Flow Breakdowns

Many SMEs are profitable on paper but still struggle to meet day-to-day obligations.

Delayed receivables create timing mismatches.

Fixed expenses continue despite uneven inflows.

Short-term borrowing increases repayment pressure.

Aligning your capital structure so stable expenses are backed by reliable funding improves financial stability, especially in sectors with longer receivable periods.

Why Financing Structure Matters

How you finance permanent working capital is as important as how much you maintain.

Lenders evaluate revenue stability and cash flow visibility.

Funding should align with predictable expense cycles.

Lower-cost options may come with more rigid structures.

Using short-term credit for permanent needs often leads to a cycle of refinancing and mounting costs. Platforms like Recur Club help businesses identify non-dilutive financing options that match their steady capital requirements, enabling better planning without compromising ownership.

Permanent vs. Temporary Working Capital

Both types of working capital are essential, but they serve different purposes in business finance. Permanent working capital provides a steady foundation, while temporary working capital supports short-term fluctuations.

Recommended: Decoding the Loan Components in Working Capital Finance.

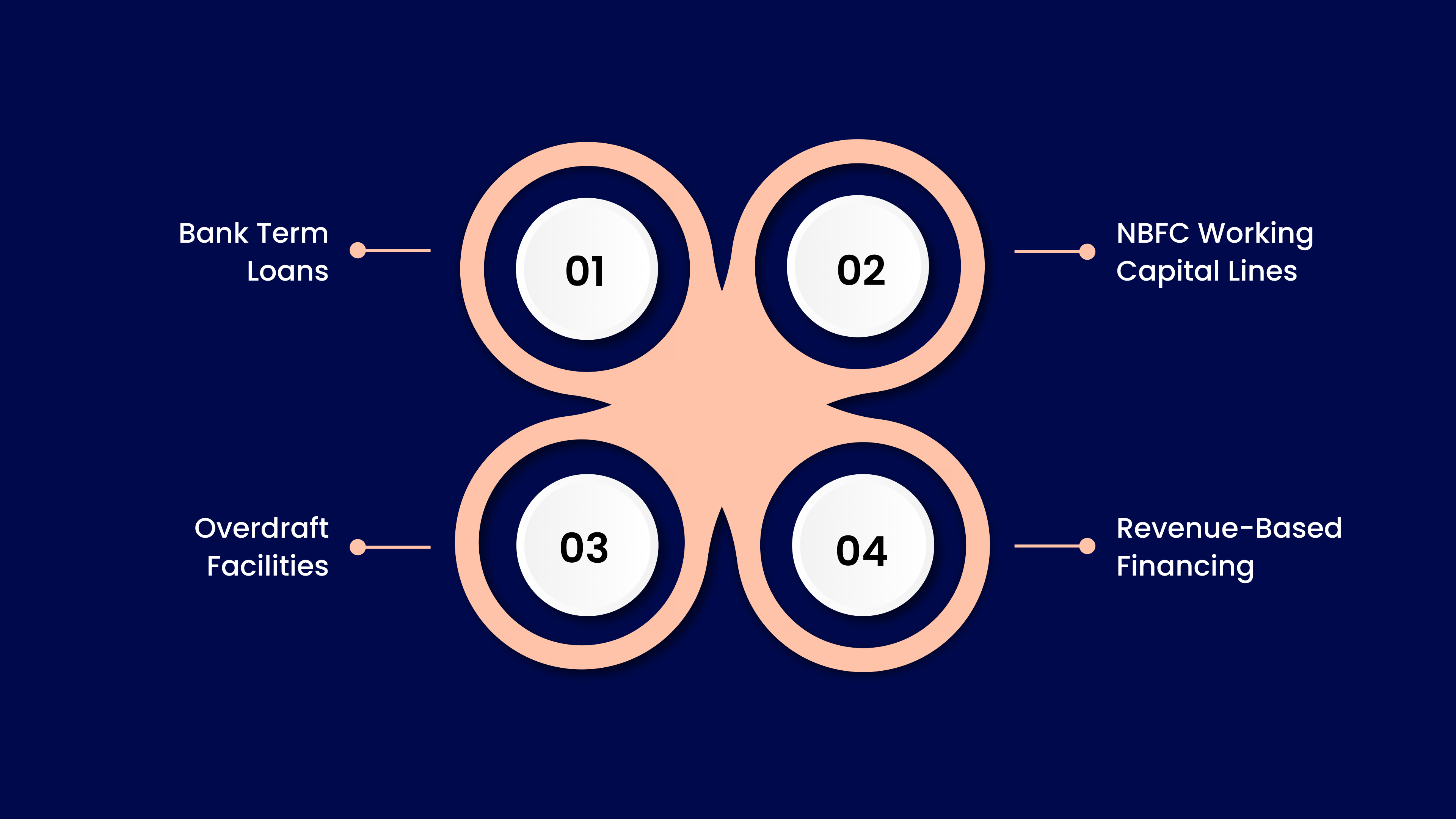

Loans and Financing Options for Permanent Working Capital

After defining and managing your working capital, the next step is securing funds to sustain it. Permanent working capital loans are designed to meet this ongoing need for reliable cash.

Common financing options include:

Bank Term Loans: Traditional banks offer long-term loans with fixed repayment schedules. These suit businesses with a strong credit history and consistent earnings, but often involve detailed documentation and collateral.

NBFC Working Capital Lines: Non-banking financial companies provide flexible funding for smaller enterprises. They are typically faster in approval but may charge higher interest rates compared to banks.

Overdraft Facilities: Offered by banks against deposits or assets, overdrafts allow businesses to withdraw more than their account balance. This option provides liquidity for short durations and ongoing needs.

Revenue-Based Financing: A newer model where repayment is linked to a company’s recurring revenue. This helps subscription-based or service-led businesses maintain cash flow without equity dilution or rigid EMIs.

Freight platform Freightify used Recur Club to access ₹14.7 crore in non-dilutive capital and tripled its monthly revenue without cash flow strain, by aligning funding with its receivables cycle.

Lenders usually assess:

Financial stability and cash-flow visibility

Credit history and repayment record

Predictability of revenue or contracts

Platforms like Recur Club enable businesses to connect with multiple capital providers and access working capital without equity dilution or lengthy bank processes.

Also Check: Top 10 Short-Term Sources of Finance to Manage Your Business Cash Flow.

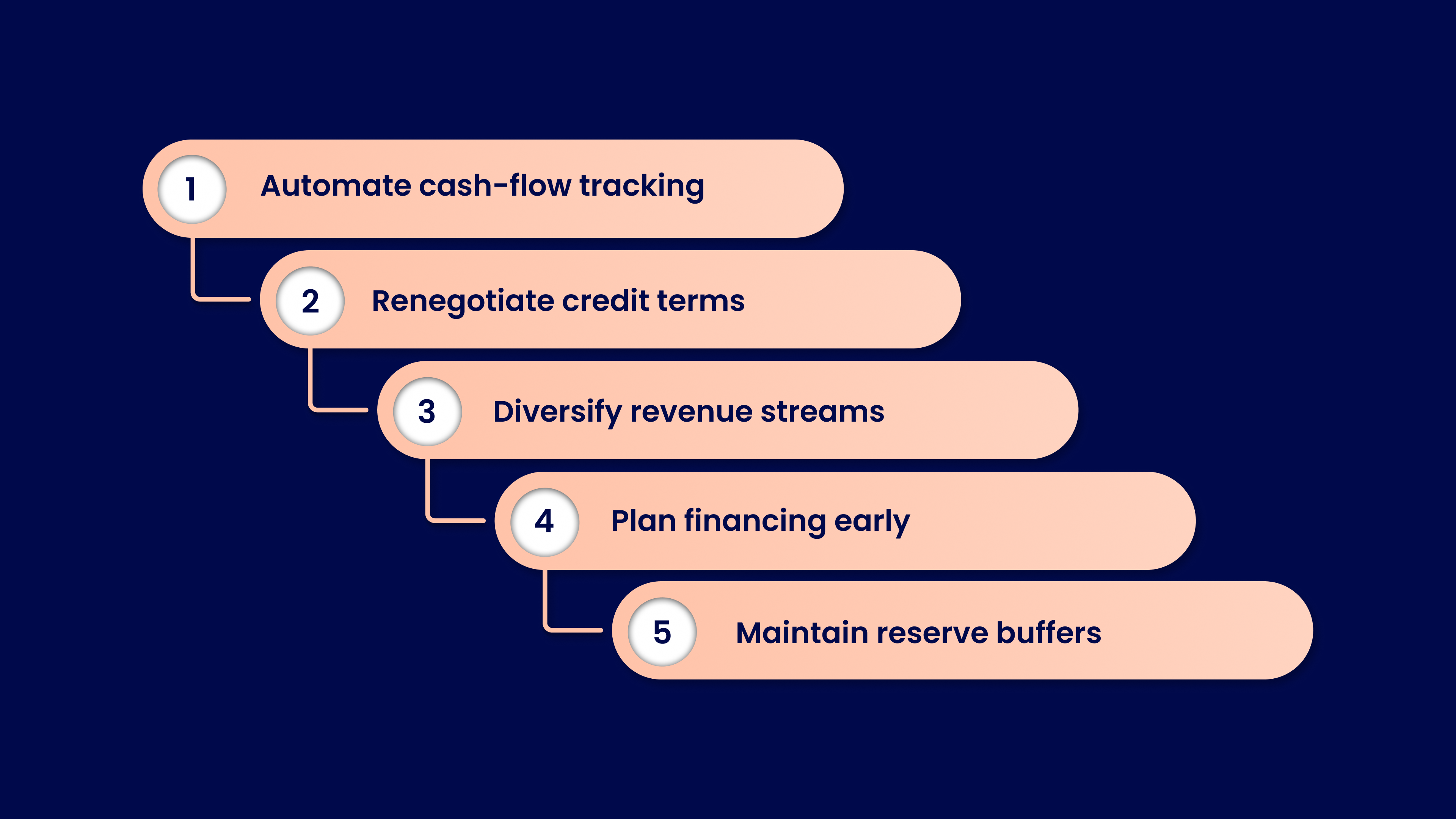

Tips to Strengthen Permanent Working Capital

Efficient management of permanent working capital helps businesses maintain stability while freeing up cash for growth. Small, consistent actions can create long-term impact. Here’s what you can do:

Automate cash-flow tracking: Use digital tools to monitor inflows and outflows in real time. Early visibility helps prevent shortfalls.

Renegotiate credit terms: Extend payment timelines with suppliers or offer small discounts for faster customer payments.

Diversify revenue streams: Relying on a single client or product increases risk. Multiple revenue sources improve liquidity.

Plan financing early: Anticipate funding needs before they become urgent. Proactive planning helps secure better credit terms and avoids last-minute borrowing.

Maintain reserve buffers: Keep a small portion of earnings aside to handle tax delays or seasonal gaps.

If you want steadier liquidity and faster access to funds, Recur Club can help you convert future revenue into immediate working capital. This gives you room to run day-to-day operations smoothly while planning growth with certainty.

Conclusion

A stable base of permanent working capital keeps businesses resilient through growth cycles and market shifts. Accessing the right funding ensures this stability without disrupting day-to-day operations.

Recur Club helps founders and finance leaders do exactly that by connecting them with trusted capital providers and enabling quick, non-dilutive access to working capital. The platform supports startups and SMEs across industries, ensuring that predictable revenues translate into financial flexibility.

Why Recur Club:

₹3,000 Cr+ in capital funded across 2,000+ customers

Backed by 100+ marquee lenders and partners, including banks, NBFCs, and AIFs

Fast, transparent access to working capital without equity dilution

Connect with us today to strengthen your capital base and fund growth with confidence.

FAQs

1. What is a permanent working capital loan?

A permanent working capital loan provides long-term funding to maintain a company’s baseline cash needs, such as inventory, payroll, and recurring expenses, throughout the year.

2. How is permanent working capital different from temporary working capital?

Permanent working capital supports ongoing operations, while temporary working capital covers short-term or seasonal requirements that fluctuate with business activity.

3. Who can apply for a permanent working capital loan in India?

Businesses with consistent revenue streams, such as SaaS startups, D2C brands, and SMEs, can apply through banks, NBFCs, or platforms like RecurClub.

4. What factors determine the loan amount for working capital?

Lenders assess cash-flow stability, receivables cycle, credit history, and growth projections before deciding the eligible loan amount.

5. How can businesses improve their permanent working capital position?

Automate collections, monitor cash flow regularly, negotiate supplier terms, and use financing platforms to maintain steady liquidity.

6. When should a business consider a permanent working capital loan?

A business should consider a permanent working capital loan when it has consistent operating expenses but faces recurring cash flow gaps due to delayed receivables or long sales cycles. It is most relevant for companies with predictable revenue but timing mismatches.

7. Is it advisable to use short-term loans for permanent working capital needs?

Using short-term loans for permanent working capital can create repayment pressure and lead to repeated refinancing. Since the need is ongoing, long-term or structured financing options are typically more suitable and cost-efficient.

8. How do lenders evaluate eligibility for permanent working capital financing?

Lenders assess factors such as revenue consistency, cash flow visibility, receivables cycle, credit history, and overall financial stability. Businesses with predictable income streams and clear repayment capacity are more likely to qualify.

Related Articles

Solving Cash Flow Gaps: The Role of Working Capital Loans for Indian Startups in 2026

Explore when a loan for working capital is useful, its key uses, and how businesses can manage expenses and growth without cash flow gaps.

Confidential Invoice Discounting: Meaning, How It Works, and When to Use It for SME Cash Flow

Understand confidential invoice discounting, how it works, costs, and when SMEs should use it for faster, non-dilutive working capital.

Capital Efficiency: Meaning, Formula, and How to Improve It for Smarter Business Growth

Learn what capital efficiency means, how to calculate it, and how founders can improve it to grow faster without wasting capital.

Talk to our experts and find the right financing solution.

Talk to Our Experts →