Debt Financing Agreements for Indian Startups: Key Terms and Negotiation Tips

What is a debt financing agreement? A practical guide for Indian startups covering covenants, repayment terms, defaults, and risks.

Debt agreements don’t usually hurt businesses upfront. The impact shows up later, when a covenant breach cuts the runway short or a collateral clause limits flexibility after raising capital.

As more startups turn to debt to fund growth without dilution, its role is expanding. Venture debt in India reached $1.3 billion in 2025, with its share in startup funding rising from 2–3% to nearly 9%.

But debt financing agreements often include terms around repayment, covenants, and penalties that aren’t obvious at first read. Before you sign, it’s worth understanding how a debt financing agreement works, which clauses matter most, and how to approach them to support scale. This guide walks you through the essentials so that debt strengthens your business rather than slowing it down.

Key Takeaways

A debt financing agreement defines repayment terms, obligations, and restrictions, not just the cost of capital.

Repayment structure and covenants directly impact cash flow and should align with your revenue cycle.

Restrictive clauses can limit future fundraising, operational decisions, and use of assets.

Defaults can be triggered by covenant breaches or compliance issues, even if repayments are on time.

Negotiating terms like repayment schedules, covenants, and collateral can significantly improve flexibility as you scale.

What Is a Debt Financing Agreement for Startups?

A debt financing agreement is a formal contract that defines how your startup borrows and repays capital. It outlines key terms such as the loan amount, interest rate, repayment schedule, covenants, and any conditions you must meet during the tenure.

While most agreements may look similar at a high level, the details determine how flexible the capital really is. The structure you sign up for will shape how repayments work, what restrictions apply, and how much control you retain as you scale.

If you’re at the stage where revenue is predictable but you want to avoid equity dilution, a revenue-linked facility like Recur Swift can help you access non-dilutive capital while keeping repayments tied to your actual inflows, instead of rigid EMIs.

Why Debt Financing Agreements Matter for Founders

Debt doesn’t just bring in capital; it introduces obligations that directly affect how your business operates. The terms in your agreement influence both day-to-day cash flow and long-term growth decisions. It can impact:

Cash flow impact: Repayment schedules and interest costs affect liquidity every month

Operational flexibility: Covenants can limit decisions like raising more capital or expanding

Future fundraising: Some clauses restrict additional debt or equity rounds

Risk exposure: Defaults can be triggered by covenant breaches, not just missed payments

A well-structured agreement supports growth without dilution. A misaligned one can create pressure at the exact moment your business needs flexibility.

Types of Debt Financing Agreements for Indian Startups

Debt financing comes in different forms, each designed for specific business needs and cash flow patterns. Choosing the right structure ensures repayments stay manageable as you grow.

Term Loans: A fixed amount borrowed for a set tenure with regular EMIs. Best for businesses with predictable cash flows.

Working Capital Loans: Short-term funding for day-to-day operations like inventory or payroll. Helps manage cash flow gaps.

Venture Debt: Debt for VC-backed startups, often alongside equity rounds. May include small equity components and growth-linked covenants.

Revenue-Based Financing (RBF): Repayments are a percentage of monthly revenue. Flexible for businesses with recurring income.

Invoice Financing: Capital raised against unpaid invoices. Improves cash flow when receivables are delayed.

The right agreement depends on your revenue model and repayment capacity.

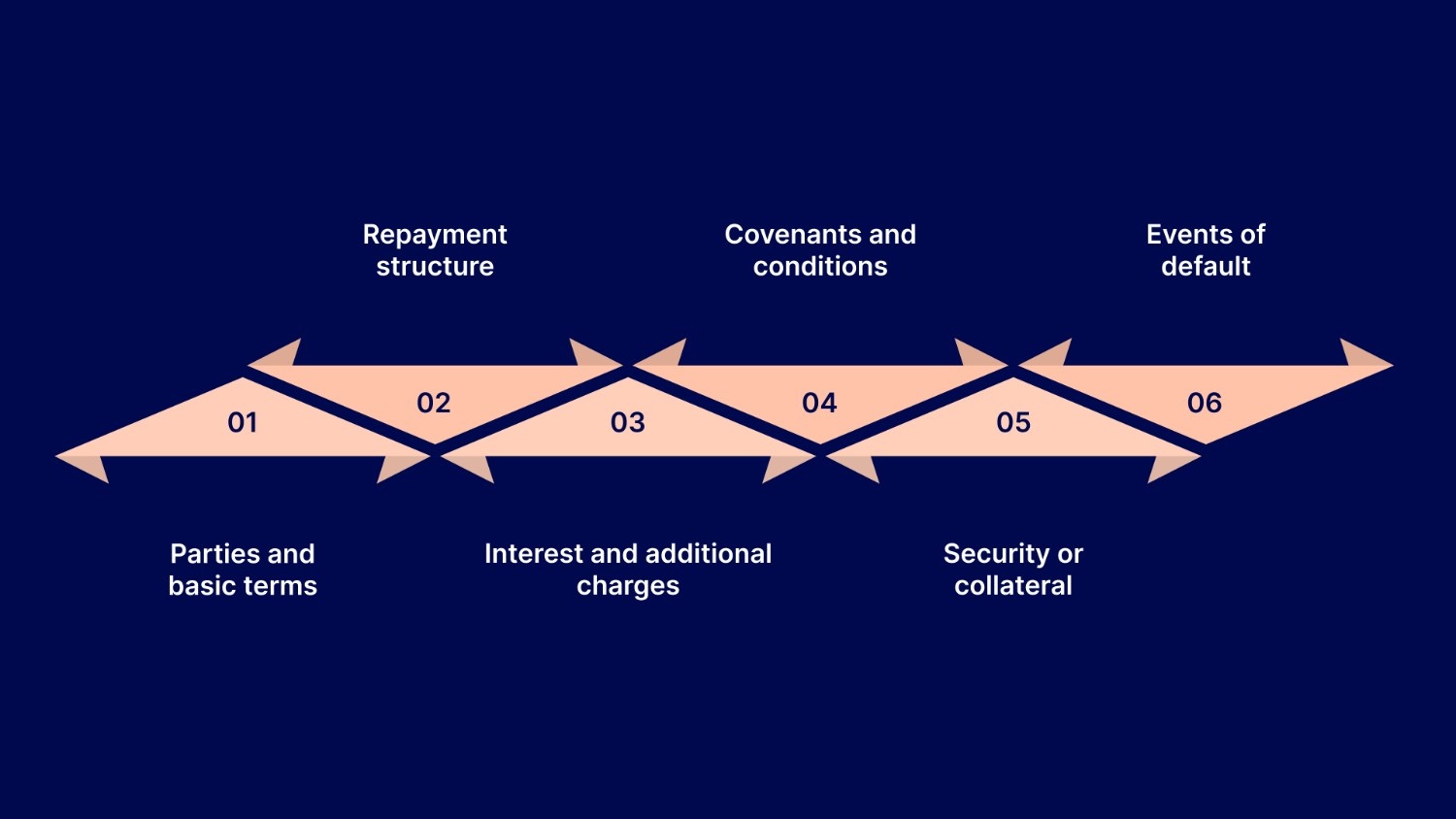

Common Sections You’ll Find in a Debt Financing Agreement

Most debt financing agreements follow a standard structure. What matters is knowing which sections directly impact your cash flow, flexibility, and future fundraising. Here are the key components to review closely:

Parties and basic terms: Identifies the borrower, lender, loan amount, tenure, and currency. It also clarifies whether the facility is term-based, revolving, or milestone-linked, which affects how the capital can be used.

Repayment structure: Defines the repayment schedule, frequency, and method. This may include EMIs, moratorium periods, or bullet payments. The structure should align with how your business generates cash.

Interest and additional charges: Covers whether the rate is fixed or floating, along with late payment charges and prepayment penalties. These terms determine the actual cost of debt beyond the headline rate.

Covenants and conditions: These are ongoing requirements such as maintaining financial ratios, limiting additional debt, or sharing regular reports. Some covenants also restrict operational or ownership changes. Breaching them can trigger penalties even if repayments are on track.

Security or collateral: Lists what backs the loan, such as business assets, receivables, or personal guarantees. While this may reduce interest rates, it can limit future borrowing if assets are already pledged.

Events of default: Defines what qualifies as a default, including missed payments, covenant breaches, or compliance issues. It also outlines lender rights, such as penalties or early repayment.

Understanding these sections helps you assess whether the agreement supports your growth or creates risks that may only surface later.

Also Read: Guide to Understanding Debt Financing for Startups

Key Repayment and Interest Terms That Affect Your Cash Flow

The real impact of debt shows up in how repayments and costs are structured. These terms directly influence your monthly cash flow and financial flexibility.

Repayment schedule: Defines how often repayments are made and in what form, such as monthly installments, bullet payments, or structured payouts. The schedule should align with your revenue cycle to avoid working capital stress.

Moratorium or grace period: Specifies whether repayments begin immediately or after a set period. A moratorium can provide breathing room while you deploy capital and stabilize cash flows.

Interest structure: Clarifies whether the rate is fixed or floating and how interest is calculated. Floating rates can increase costs over time, while fixed rates offer predictability.

Penalties and prepayment terms: Covers late payment charges and conditions for early repayment. These terms affect flexibility and determine how costly it is to close the loan ahead of schedule.

Reviewing these elements together helps ensure repayments remain predictable as your business grows. For startups in a growth phase, structuring these terms correctly is critical. Solutions like Recur Scale are designed to align repayment schedules and cost structures with your cash flows, so debt supports scale instead of constraining it.

Also Read: Venture Debt Due Diligence for Businesses: How to Prepare and Succeed

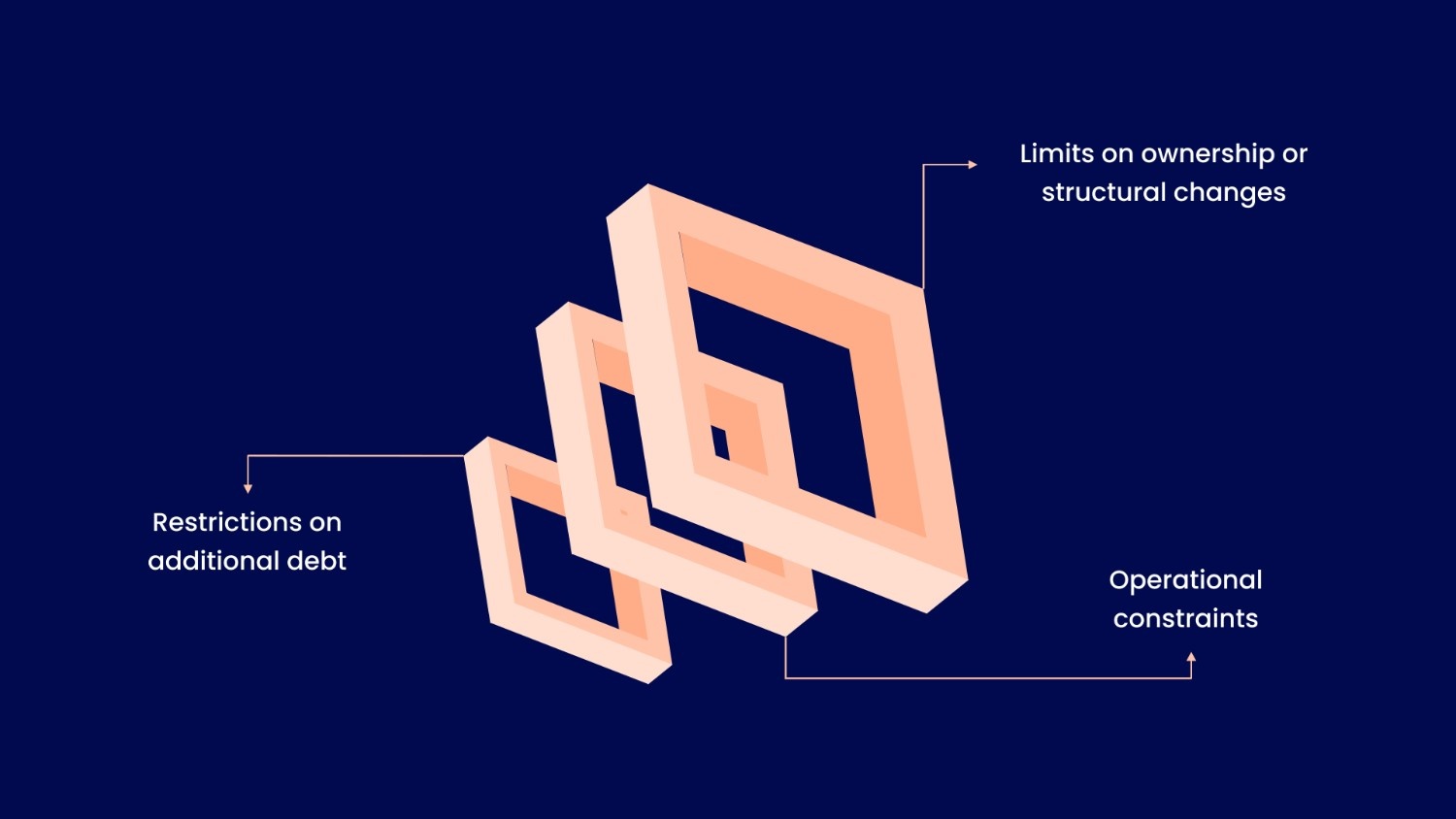

Terms That Can Restrict Your Business Operations

Beyond repayments, some clauses directly affect how freely you can run and grow your business.

Restrictions on additional debt: Many agreements limit your ability to raise more debt without lender approval. This can slow future fundraising even when the business is performing well.

Limits on ownership or structural changes: Clauses may restrict changes in shareholding, mergers, or acquisitions. These are important if you’re planning future equity rounds or strategic moves.

Operational constraints: Certain agreements require lender consent for major business decisions, asset sales, or expansion into new lines. This can reduce agility during growth phases.

Reviewing these limits upfront helps you avoid agreements that quietly constrain scale.

What Happens When a Default Is Triggered

Defaults are not limited to missed repayments. Many founders underestimate how easily they can be triggered.

Payment-related defaults: Missing or delaying repayments beyond the allowed window

Covenant breaches: Failing to meet financial or operational conditions, even temporarily

Compliance or disclosure issues: Delays in reporting, incorrect information, or legal issues

Once triggered, defaults can lead to penalties, higher costs, or accelerated repayment. Reviewing these triggers in advance helps you assess risk more accurately before signing.

How to Review and Negotiate a Debt Financing Agreement

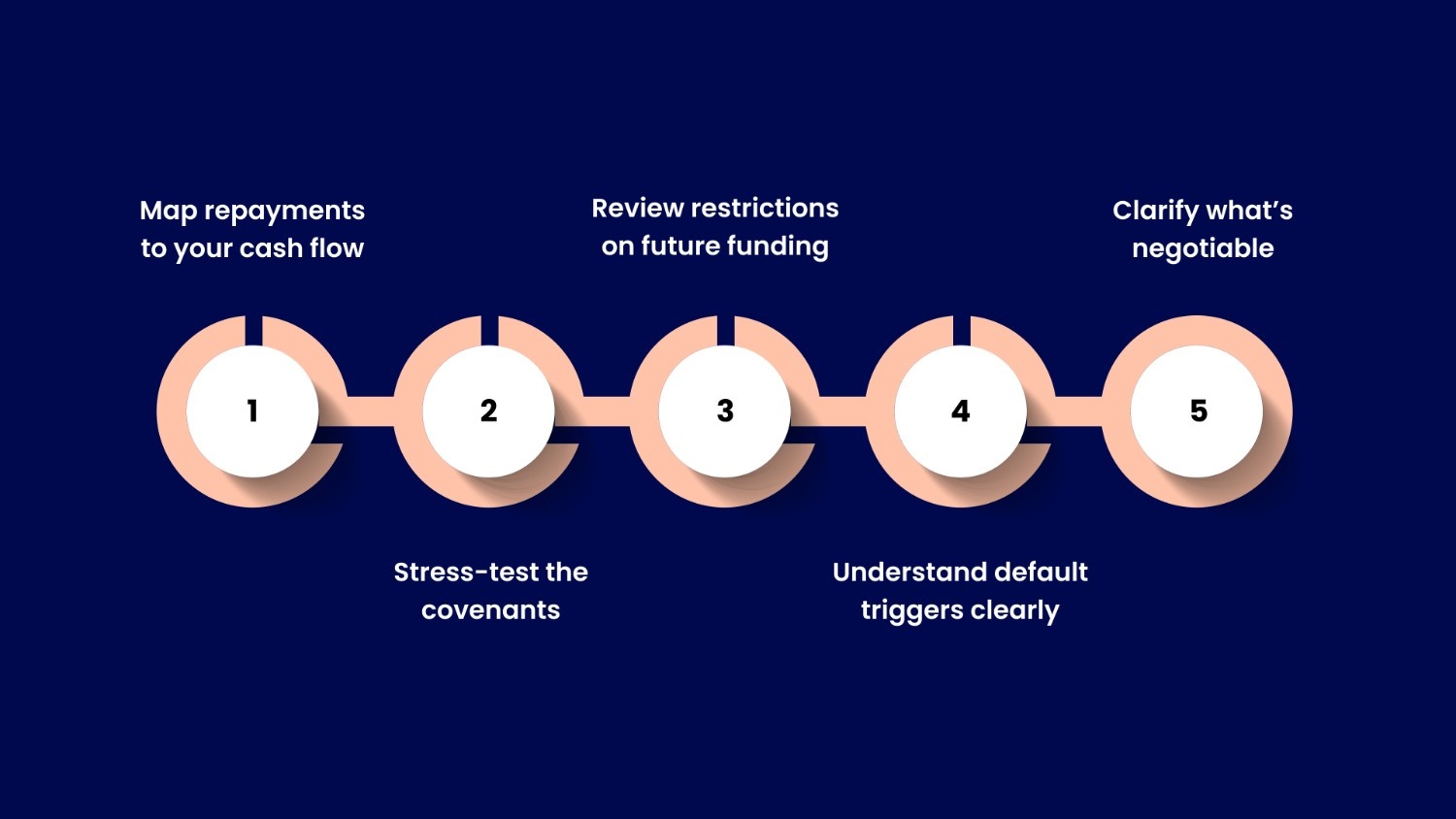

Before committing, the goal isn’t to eliminate risk, but to ensure the agreement fits how your business operates. A structured approach helps you avoid surprises and negotiate better terms.

Step 1: Map repayments to your cash flow

Review repayment schedules alongside your revenue cycle. Monthly repayments may work for predictable SaaS revenue, but can strain businesses with seasonal or uneven inflows.

Step 2: Stress-test the covenants

Assess what happens if revenue dips, collections slow, or expenses spike for a quarter. If a covenant is easy to breach during normal fluctuations, it’s a risk, not a safeguard.

Step 3: Review restrictions on future funding

Check whether the agreement limits additional debt, equity raises, or asset usage. These clauses matter if you plan to raise capital or expand in the next 12–18 months.

Step 4: Evaluate default triggers carefully

Don’t assume default only means missed payments. Confirm whether reporting delays, covenant breaches, or compliance issues can trigger penalties or early repayment.

Step 5: Negotiate key terms

Many terms are flexible, especially if your business has stable revenue. Focus on:

Repayment timelines that match your cash flow

Covenant thresholds with reasonable headroom

Lower or no prepayment penalties

Reduced collateral or removal of personal guarantees (where possible)

These changes can improve flexibility as you scale. Taking this approach helps ensure the agreement supports your growth without creating unnecessary pressure.

Choosing the right lender is just as important as negotiating the right terms. Not all debt is structured the same, and mismatched terms can create constraints later. Recur Club works as a debt marketplace and capital partner, helping Indian startups and SMEs connect with lenders offering debt structures aligned with their cash flows, so founders don’t have to navigate opaque terms alone.

Conclusion

Debt can be a powerful growth tool when the agreement behind it is clear, balanced, and aligned with how your business operates. The real risk isn’t debt itself, it’s signing terms that don’t match your cash flow, growth timeline, or future funding plans.

With the right structure and visibility into key clauses, debt can extend runway, fund expansion, and support scale without dilution. The goal is not just to raise capital, but to raise it on terms that work for your business.

If you’re evaluating debt and want clarity on terms before you commit, Recur Club can help you approach the process with confidence.

As a debt marketplace and capital partner, Recur Club helps your business:

Access non-dilutive capital from 150+ institutional lenders

Get advisory-led matching based on your cash flows

Move quickly, with approvals possible in as little as ~48 hours

Talk to our capital advisors today!

Frequently Asked Questions

1. What is the difference between a loan agreement and a debt financing agreement?

A loan agreement usually refers to a single borrowing facility. A debt financing agreement is broader; it may include multiple facilities, structured repayments, covenants, and conditions tied to business performance.

2. Can a covenant breach trigger repayment even if EMIs are on time?

Yes. Many agreements allow lenders to act on covenant breaches independently of repayment history, which is why these clauses need close review.

3. Does signing a debt agreement affect future fundraising?

It can. Some agreements restrict additional debt, require lender consent for equity raises, or pledge assets that future investors may expect to remain unencumbered.

4. How do founders compare debt offers beyond interest rates?

Founders should compare repayment flexibility, covenant strictness, collateral requirements, default triggers, and prepayment terms, not just the headline cost.

5. Can startups negotiate debt financing agreement terms?

Yes. Many terms in a debt financing agreement are negotiable, especially for startups with stable revenue or strong growth. Founders can often negotiate repayment schedules, covenant thresholds, prepayment penalties, and collateral requirements to better align with their cash flows.

Related Articles

Proforma Invoice Financing: How Businesses Fund Orders Before Billing

Proforma invoice financing helps fund orders before billing. Learn uses, format, examples, and how businesses manage upfront costs effectively.

Financial Forecasting for Startups: Build Projections That Help You Raise Capital

Master financial forecasting for startups with revenue, expense, and cash flow projections to plan growth and attract investors.

B2B Lending Explained: A Practical Guide for Indian SMEs

Understand B2B lending meaning, how it works, types, and when SMEs should use it for faster, non-dilutive business financing.

Talk to our experts and find the right financing solution.

Talk to Our Experts →