Solving Cash Flow Gaps: The Role of Working Capital Loans for Indian Startups in 2026

Explore when a loan for working capital is useful, its key uses, and how businesses can manage expenses and growth without cash flow gaps.

In 2026, many Indian SMEs and startups are winning customers and closing sales, yet still struggle to keep cash flowing through the business cycle. A major reason is that billions of rupees in receivables remain unpaid for far too long, choking liquidity and slowing growth.

According to the Economic Survey 2025‑26, an estimated ₹8.1 lakh crore is stuck in delayed payments, severely restricting working capital for businesses across sectors.

With India’s broader economy still growing strongly, this working capital gap is emerging as one of the biggest internal hurdles for agile businesses that need funds fast to hire, innovate, and expand. In this blog, you will learn how to navigate the cash‑flow crunch and make financing work for your business.

Quick Overview

Working capital loans help businesses manage liquidity gaps caused by delayed payments and seasonal fluctuations, ensuring smooth operations.

Immediate funds from working capital loans allow SMEs and startups to expand inventory, invest in marketing, and seize new business opportunities.

Regular and timely repayment of working capital loans can improve a business’s credit score, making it easier to secure future financing at better rates.

These loans provide flexibility for a variety of business needs, such as paying staff salaries, covering utility bills, and purchasing raw materials.

Recur Club helps startups and SMEs connect with potential lenders, offering them access to recurring working capital based on future revenue, ensuring continuous business growth.

What Is a Working Capital Loan?

A loan for working capital is a short-term financing option that helps businesses manage day-to-day expenses when cash inflows are delayed or uneven. It supports ongoing business needs rather than long-term investments like machinery or infrastructure.

For SMEs, it ensures operations continue smoothly during cash flow gaps. Working capital loans are closely linked to a business’s cash conversion cycle, especially when receivables and payables are not aligned. These loans are typically repaid over a shorter tenure and aligned with cash flow patterns, making them suitable for immediate funding needs.

Why Working Capital Loans Still Matter in 2026

Big credit gap still limits scaling

Despite strong demand, many Indian small businesses continue to face a working capital and credit gap of around ₹20–25 lakh crore, making it harder to fund day‑to‑day needs and growth.Slow payments squeeze cash flow

Customers, especially larger corporations, frequently take much longer than agreed to pay, leaving businesses with less usable cash when expenses are due.Daily costs don’t wait for revenue

Even profitable startups can run into trouble because salaries, supplier bills, rent and other fixed costs must be paid before cash arrives from clients, creating real‑world liquidity stress.Seasonal demand increases upfront spend

Peak periods like festive seasons and wedding months bring extra demand but also require large upfront investments in inventory, staffing and marketing before revenues arrive.Traditional loans are slow and rigid

Banks often require extensive documentation, collateral and long approval times, which means businesses miss time‑sensitive opportunities while waiting for funds.

When a Working Capital Loan Makes Sense for Your Business

Businesses often need a working capital loan when there is a gap between outgoing expenses and incoming revenue, especially during growth phases or uneven cash flow.

Typical scenarios include:

Delayed customer payments: Revenue is booked, but cash hasn’t been received

Seasonal sales cycles: Funds needed to prepare for peak demand

Large purchase orders: Upfront spending required to fulfil bulk orders

Inventory stocking: Buying in advance to avoid stockouts or secure better pricing

Expansion marketing: Upfront spend on campaigns before returns are realised

One practical example is WeVOIS, an environmental services and SaaS company based in Jaipur. When traditional funding was slow and inflexible, they partnered with a fast capital provider Recur Club and received flexible debt financing within 48 hours, raising a total of ₹7.3 crore.

With this working capital support, WeVOIS grew revenue 2.7×, improved EBITDA, and expanded into six new cities, all while delaying equity fundraising until they could secure a stronger valuation.

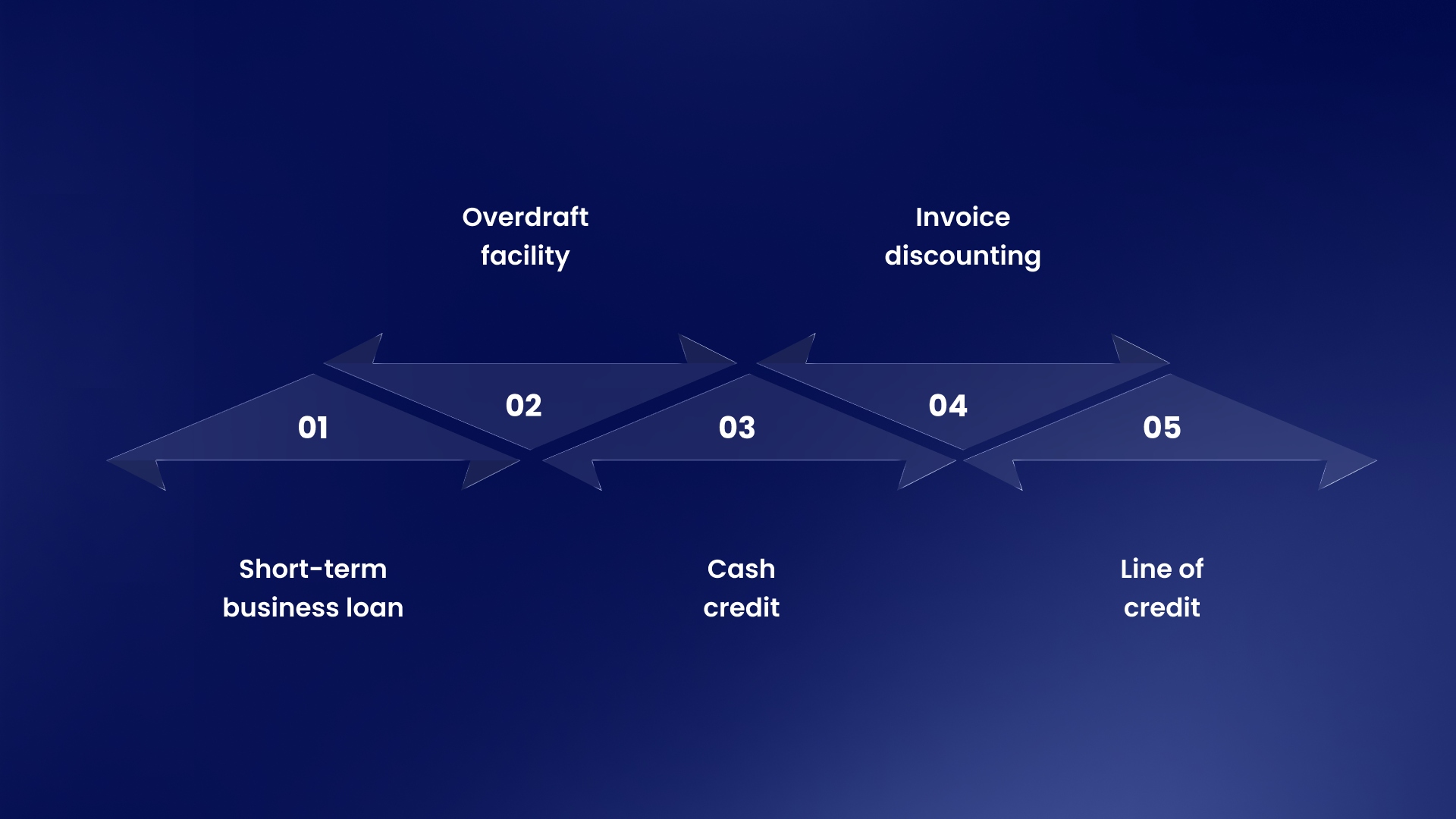

Types of Working Capital Loan Solutions

Businesses can choose from different types of working capital financing based on their cash flow patterns and funding needs.

Short-term business loan: A fixed amount borrowed for a short duration, usually repaid in instalments. Suitable for immediate expenses or planned short-term requirements.

Overdraft facility: Allows businesses to withdraw more than their account balance up to a limit. Interest is charged only on the amount used.

Cash credit: A flexible funding option where businesses can draw funds against inventory or receivables. Commonly used to manage ongoing working capital needs.

Invoice discounting: Enables businesses to access funds against unpaid invoices. This helps improve cash flow without waiting for customer payments.

Line of credit: Provides access to a pre-approved limit that can be used as needed. Businesses can withdraw, repay, and reuse funds based on requirements.

Working Capital Loan vs Term Loan: Which One Suits Your Business Needs?

Suggested Read: Understanding Secured Loans: Types, Benefits, & How to Apply

How a Working Capital Loan Functions: A Step-by-Step Guide

When applying for a working capital loan through Recur Club, the process is designed to be quick, transparent, and tailored to your business's cash flow needs. Here’s how the process works:

1. Loan Application

Start by submitting a simple digital application, where you provide essential business details, including financial data, cash flow history, and other key information.

The AI-powered system analyses your financials to determine eligibility and matches you with the most appropriate loan product based on your needs.

2. Loan Approval

Your business’s cash flow patterns and overall financial health are evaluated using real-time data. This AI-driven assessment speeds up the approval process compared to traditional methods.

You can get approved for unsecured loans or loans secured against your receivables or inventory, depending on your preference and business situation.

3. Disbursement of Funds

Once approved, funds are disbursed quickly, typically within 48 hours, and are transferred directly to your bank account for immediate access to capital.

4. Repayment Structure

The repayment terms are flexible and aligned with your business’s revenue cycle.

Fixed Installments: Some loan options offer fixed monthly payments.

Revenue-Linked Repayments: Other options allow for payments tied to your revenue generation, so you repay when the funds are available.

5. Loan Closure

Once the loan is fully repaid, the agreement is closed, and you’re free from debt obligations, allowing you to continue focusing on business growth without the burden of complicated loan management.

Suggested Read: Underwriting Small Business Loans: Process, Criteria, and How to Improve Approval Chances

Eligibility and Documents for a Working Capital Loan

To apply for a working capital loan, the following documents are typically required:

Eligibility Criteria

To qualify for a working capital loan, businesses generally need to meet the following eligibility criteria:

What Determines the Cost of a Working Capital Loan?

The cost of a working capital loan depends on how the funding is structured and how well it aligns with your cash flow. For SMEs, it’s important to look beyond just the interest rate and evaluate the overall cost of borrowing.

Key factors include:

Interest rate: Interest rates on working capital loans vary based on the lender, business profile, and type of financing. For most SMEs, rates typically range from around 10% to 24% annually.

Processing and platform fees: One-time charges that impact the total cost.

Repayment structure: Fixed EMIs vs flexible repayments can affect cash flow and effective cost.

Loan tenure: Shorter tenures may have higher instalments but lower total interest outflow.

Before choosing a loan, businesses should assess whether the expected returns from using the funds justify the cost, especially for short-term or revenue-linked needs.

How to Calculate Working Capital Ratio and Its Role in Deciding on a Loan

Working Capital Ratio is a key financial metric used to evaluate a business's short-term liquidity. It measures a company's ability to pay off its short-term liabilities with its short-term assets. This ratio can help businesses decide whether a working capital loan is necessary to maintain smooth operations.

Formula to Calculate Working Capital Ratio:

Working Capital Ratio = Current Assets ÷ Current Liabilities

Where:

Current Assets: Assets that are expected to be converted into cash within a year (e.g., cash, receivables, inventory).

Current Liabilities: Obligations that need to be settled within a year (e.g., short-term debts, payables).

How to Interpret the Working Capital Ratio:

Ratio > 1: The business has more assets than liabilities and is generally in a good financial position to meet short-term obligations.

Ratio = 1: The business has just enough assets to cover its liabilities, indicating a break-even scenario.

Ratio < 1: The business might face liquidity issues and could struggle to pay its short-term debts.

How This Helps in Deciding on a Working Capital Loan:

Low Ratio (<1): A working capital ratio below 1 indicates a potential liquidity crisis. Your business may be unable to cover day-to-day operational costs, and this is a clear signal that a working capital loan could help bridge the gap and ensure business continuity.

Ratio ~ 1: If your ratio is close to 1, it’s a warning that your business could become cash-strapped during periods of high expenditure (e.g., seasonal demand). A working capital loan can provide a buffer when cash flow is tight but not completely negative.

High Ratio (>1): If your ratio is above 1, your business is likely in a strong liquidity position. However, if you're aiming to expand, the extra working capital could be used more efficiently for growth rather than sitting idle. A loan might still be useful for taking advantage of opportunities like bulk purchasing, marketing campaigns, or new hires.

Practical Scenario:

Imagine your business has:

Current Assets of ₹50,00,000

Current Liabilities of ₹30,00,000

The Working Capital Ratio would be: ₹50,00,000 ÷ ₹30,00,000 = 1.67

With a ratio of 1.67, your business is in a good position to pay off its short-term liabilities. However, if the ratio were below 1, a working capital loan would be a prudent decision to keep operations smooth.

How Recur Club Helps Businesses Access Working Capital

Recur Club enables businesses to access working capital through flexible, non-dilutive financing, allowing founders to raise funds without giving up equity. The platform is designed to match funding structures with real business needs, especially for companies managing uneven cash flows or growth-related expenses.

Key benefits include:

Non-dilutive capital: Raise funds without equity dilution, preserving ownership

Lender network: Access to multiple lenders, helping businesses find suitable financing options

Fast funding: Quick approval and disbursal to meet immediate business requirements

Structured repayment: Repayment plans aligned with cash flow cycles to reduce financial strain

Conclusion

A loan for working capital works best when it is used with a clear purpose covering short-term gaps, fulfilling demand, or supporting revenue-generating activities. The real impact comes from matching the right financing type with your cash flow cycle, so repayments remain manageable while the business continues to grow.

Recur Club helps businesses access non-dilutive working capital with structures suited to their needs. Connect with us today to identify the right funding option and keep your business moving forward without cash flow disruptions.

FAQs

1. Can a startup qualify for a working capital loan?

Yes, startups can qualify for a working capital loan depending on their business plan, cash flow, credit score, and other financial indicators. Lenders may be more lenient towards startups with a solid business model and a promising future.

2. How long does it take to get approval for a working capital loan?

The approval process for working capital loans can range from a few hours to a few days, depending on the lender’s requirements. Digital lenders often offer quicker approvals compared to traditional banks, especially if you meet the eligibility criteria.

3. What is the minimum turnover required to qualify for a working capital loan?

While the required turnover varies by lender, most financial institutions typically require a minimum annual turnover ranging from ₹10 lakhs to ₹1 crore for SME and startups.

4. Can I get a working capital loan if my business doesn’t have assets?

Yes, unsecured working capital loans are available for businesses without assets. However, these loans may come with higher interest rates and stricter eligibility criteria, such as a strong credit score or a proven business track record.

5. How does a working capital loan affect my credit score?

A working capital loan, like any other loan, will impact your credit score based on how well you manage the loan. Timely repayment can improve your score, while defaults or delayed payments can lower it.

6. Can I use a working capital loan to pay off other business debts?

Yes, you can use a working capital loan to pay off short-term debts, provided you have the lender's approval. However, it is important to clarify with the lender whether such use is permitted under the loan agreement.

7. What is the difference between a working capital loan and an overdraft facility?

A working capital loan is a lump-sum loan disbursed for a fixed period, typically used to cover business expenses, while an overdraft facility is a revolving line of credit allowing you to withdraw beyond your account balance, up to an agreed limit, and pay interest only on the amount used.

8. Are working capital loans offered to new businesses with no financial history?

Yes, some lenders offer working capital loans to new businesses with little or no financial history, based on alternative evaluation methods such as a strong business plan, the founder's creditworthiness, and projected cash flow.

9. Can I get a working capital loan without providing personal guarantees?

Some lenders offer unsecured working capital loans that don’t require personal guarantees, but they might come with higher interest rates and lower loan amounts. It’s important to understand the terms before agreeing to an unsecured loan.

10. Can a working capital loan help with seasonal cash flow issues?

Yes, working capital loans are often ideal for businesses facing seasonal cash flow fluctuations. They help bridge the gap between inventory purchases and sales, especially during peak seasons.

Related Articles

Confidential Invoice Discounting: Meaning, How It Works, and When to Use It for SME Cash Flow

Understand confidential invoice discounting, how it works, costs, and when SMEs should use it for faster, non-dilutive working capital.

Capital Efficiency: Meaning, Formula, and How to Improve It for Smarter Business Growth

Learn what capital efficiency means, how to calculate it, and how founders can improve it to grow faster without wasting capital.

Types of SME Loans in India: A Practical Guide to Choosing the Right Financing for Your Business

Explore types of SME loans in India, how they work, and how to choose the right one based on your business cash flow and funding needs.

Talk to our experts and find the right financing solution.

Talk to Our Experts →