What Is the Mudra Loan Scheme? Benefits, Eligibility & How to Apply in 2026

Learn what the Mudra Loan Scheme is, its benefits, eligibility criteria, loan categories, required documents, and how Indian businesses can apply for funding.

Securing business funding in India still comes with slow approvals, rigid lending requirements, and limited financing flexibility. To improve access to formal credit, the Pradhan Mantri Mudra Yojana has already supported over 57 crore loan accounts amounting to ₹40.07 lakh crore.

While the scheme has helped millions of entrepreneurs access capital, it may not always align with the needs of fast-growing startups and scaling companies. This guide explains the Mudra Loan Scheme, its benefits, eligibility criteria, application process, and alternative funding options for growing businesses.

What you need to know:

The Mudra Loan scheme helps small businesses access collateral-free funding through banks and NBFCs. It was introduced to improve formal credit accessibility across India.

Loan categories include Shishu, Kishore, Tarun, and Tarun Plus. Each category supports different business stages and funding requirements.

Eligibility depends on business activity, documentation, and repayment capability. Lenders may also evaluate cash flow stability and operational history.

Growing startups may outgrow traditional Mudra loan limits over time. Expansion costs and working capital needs often require larger financing structures.

Alternative financing models can support businesses as their capital requirements change. Common options include venture debt, invoice financing, and revenue-based funding.

What Is the Mudra Loan Scheme?

The Pradhan Mantri Mudra Yojana (PMMY) is a government-backed lending scheme designed to improve access to business funding for small and micro enterprises in India. Introduced in 2015, the scheme allows eligible businesses to access collateral-free loans through banks, NBFCs, microfinance institutions, and other approved lenders.

Mudra loans are commonly used by early-stage businesses for:

working capital requirements

inventory purchases

equipment financing

business expansion

operational expenses

While the scheme primarily targets micro and small enterprises, many founders explore Mudra loans during the early stages of building a business due to lower borrowing barriers and easier access to formal credit.

Suggested Read: Government Loan Schemes for Small Business Funding in India

Benefits of Mudra Loans for Entrepreneurs and Small Businesses

The Pradhan Mantri Mudra Yojana was introduced to improve access to formal business credit for entrepreneurs and small businesses across India. By offering collateral-free financing through banks, NBFCs, and participating lenders, the scheme aims to make business funding more accessible for businesses with smaller capital requirements.

Some of the key benefits of Mudra loans include:

No Collateral: Most Mudra loans do not require businesses to pledge assets as security, lowering borrowing barriers for entrepreneurs.

Formal Credit: The scheme helps businesses establish formal borrowing relationships with banks and financial institutions.

Flexible Usage: Mudra loans can be used for inventory purchases, equipment financing, working capital, and operational expenses.

Multiple Categories: Businesses can apply for different funding tiers based on their stage and financing requirements.

Financial Inclusion: The scheme improves credit accessibility for underserved entrepreneurs and smaller enterprises across sectors.

Women Support: Some lenders may offer concessional rates for women entrepreneurs under the scheme.

Despite schemes like Mudra, India’s MSME sector still faces an estimated credit gap of over ₹30 lakh crore, according to Small Industries Development Bank of India (SIDBI). This funding gap has pushed many growing startups and scaling businesses to explore alternative financing models with faster approvals and more flexible capital structures.

Recur Club helps growing startups access non-dilutive capital through flexible financing models and multiple lending partners. This can be useful for businesses that need faster or larger-scale funding beyond traditional MSME loan structures.

Types of Mudra Loans Under PMMY

The Pradhan Mantri Mudra Yojana divides business loans into three categories based on the stage, scale, and funding requirements of the business. These categories are designed to support businesses ranging from first-time entrepreneurs to more established small enterprises looking to expand operations.

The right Mudra loan category depends on factors such as business stage, operational scale, repayment capacity, and funding requirements.

Suggested Read: What Is a Start-Up Loan Scheme in India? Eligibility, Types, and Common Mistakes

Which Startups Are Eligible for Mudra Loan Scheme?

Eligibility criteria can vary slightly across lenders, but most banks and NBFCs evaluate factors such as business activity, funding requirements, repayment capacity, and documentation before approving a Mudra loan.

Businesses that commonly qualify for Mudra loans include:

Retail Stores: Small shops, local retailers, and trading businesses seeking working capital or inventory funding.

Service Businesses: Salons, repair centres, agencies, consultants, and other service-based businesses with operational funding needs.

Manufacturing Units: Small-scale manufacturers looking to purchase machinery, raw materials, or expand production capacity.

Food Businesses: Restaurants, cloud kitchens, bakeries, and food vendors managing operational or expansion expenses.

Transport Operators: Businesses involved in commercial transport, logistics, or delivery services.

Early Startups: Some early-stage startups with smaller funding requirements and basic operational history may also qualify.

The PM loan for business is designed for non-corporate small businesses and entrepreneurs looking to access formal business financing. As businesses grow, however, funding requirements often become more complex than traditional small-ticket loan structures can support.

How to Apply for a Mudra Loan?

Businesses can apply for a Mudra loan amount through online and offline modes. While the exact process may vary across institutions, most applications follow a similar structure involving eligibility checks, documentation, and financial assessment.

The process for applying for a Mudra startup loan is:

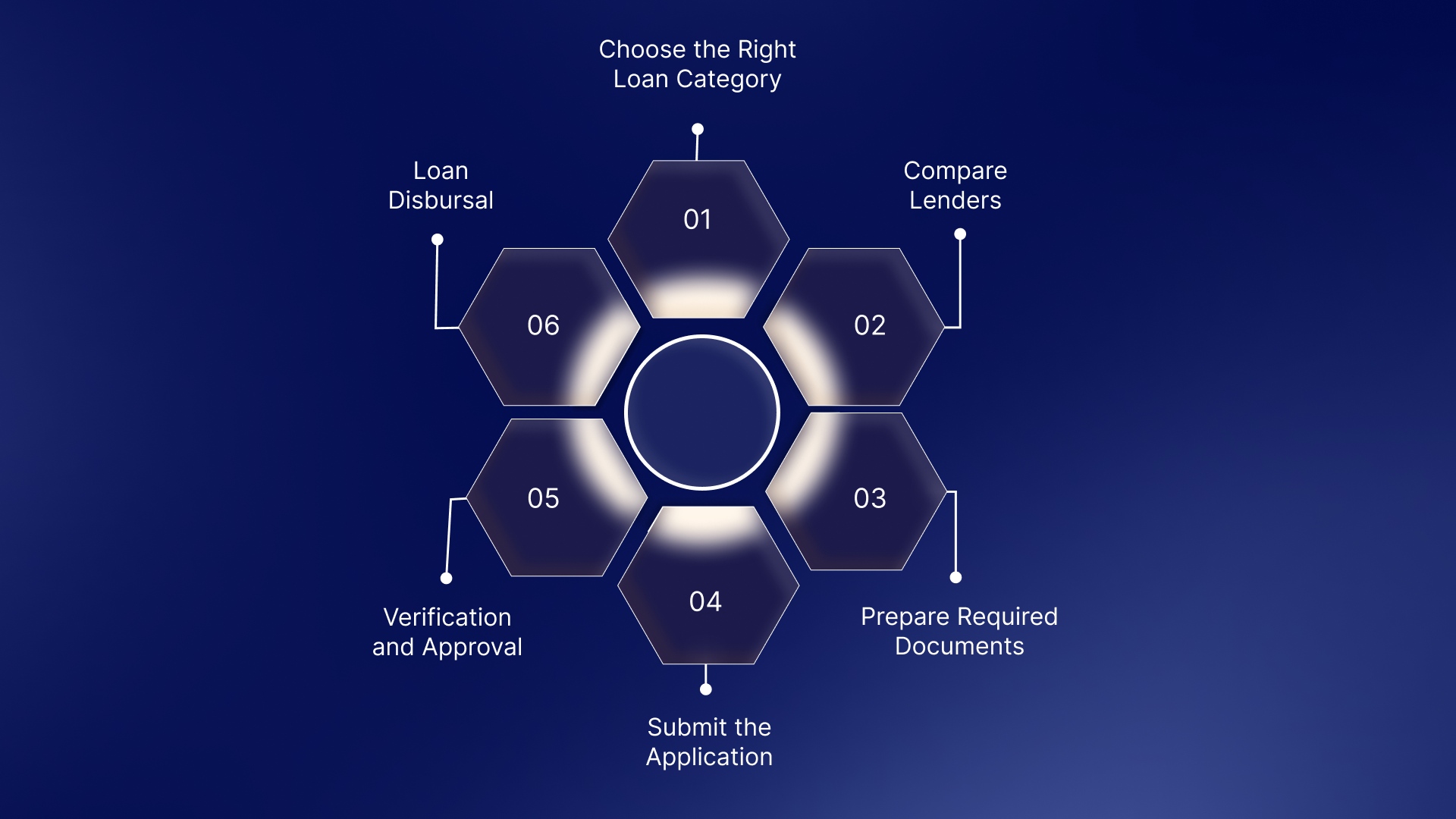

1. Choose the Right Loan Category

Businesses must first identify the appropriate Mudra loan category based on their funding requirements and stage of operations. Selecting the right category can improve approval clarity and repayment planning.

The three categories include:

Shishu: Up to ₹50,000

Kishore: ₹50,000 to ₹5 lakh

Tarun: ₹5 lakh to ₹10 lakh

2. Compare Lenders

Different lenders may have varying documentation requirements, processing timelines, and internal eligibility criteria. Comparing lenders can help businesses identify financing options better aligned with their operational needs.

Businesses can apply through:

Public sector banks

Private banks

NBFCs

Regional rural banks

Microfinance institutions

3. Prepare Required Documents

Most lenders require businesses to submit identity, business, and financial documents during the application process. Incomplete documentation can delay approvals and verification timelines.

Commonly required documents include:

Aadhaar card

PAN card

Address proof

Business registration proof

Bank statements

Income or financial records

Business plan or project details

Passport-size photographs

4. Submit the Application

Applications can usually be submitted online or offline, depending on the lender. Businesses may also need to provide details about business activity, funding requirements, and repayment plans during submission.

5. Verification and Approval

Lenders typically review business eligibility, financial stability, repayment capability, and documentation before approving the loan. Approval timelines can vary depending on the lender and the complexity of the application.

6. Loan Disbursal

Once approved, the sanctioned amount is disbursed to the borrower’s account based on the lender’s process and loan terms. Businesses can then use the funds for approved operational or growth-related requirements. Repayment tenures may extend up to 7 years, depending on the lender, loan category, and borrower profile.

While Mudra loans can support smaller funding requirements, growing startups often face additional financing challenges as operational costs, expansion plans, and working capital needs increase.

Suggested Read: Top Sources of Startup Financing for Entrepreneurs in 2026

Funding Challenges Growing Startups Face With Mudra Loans

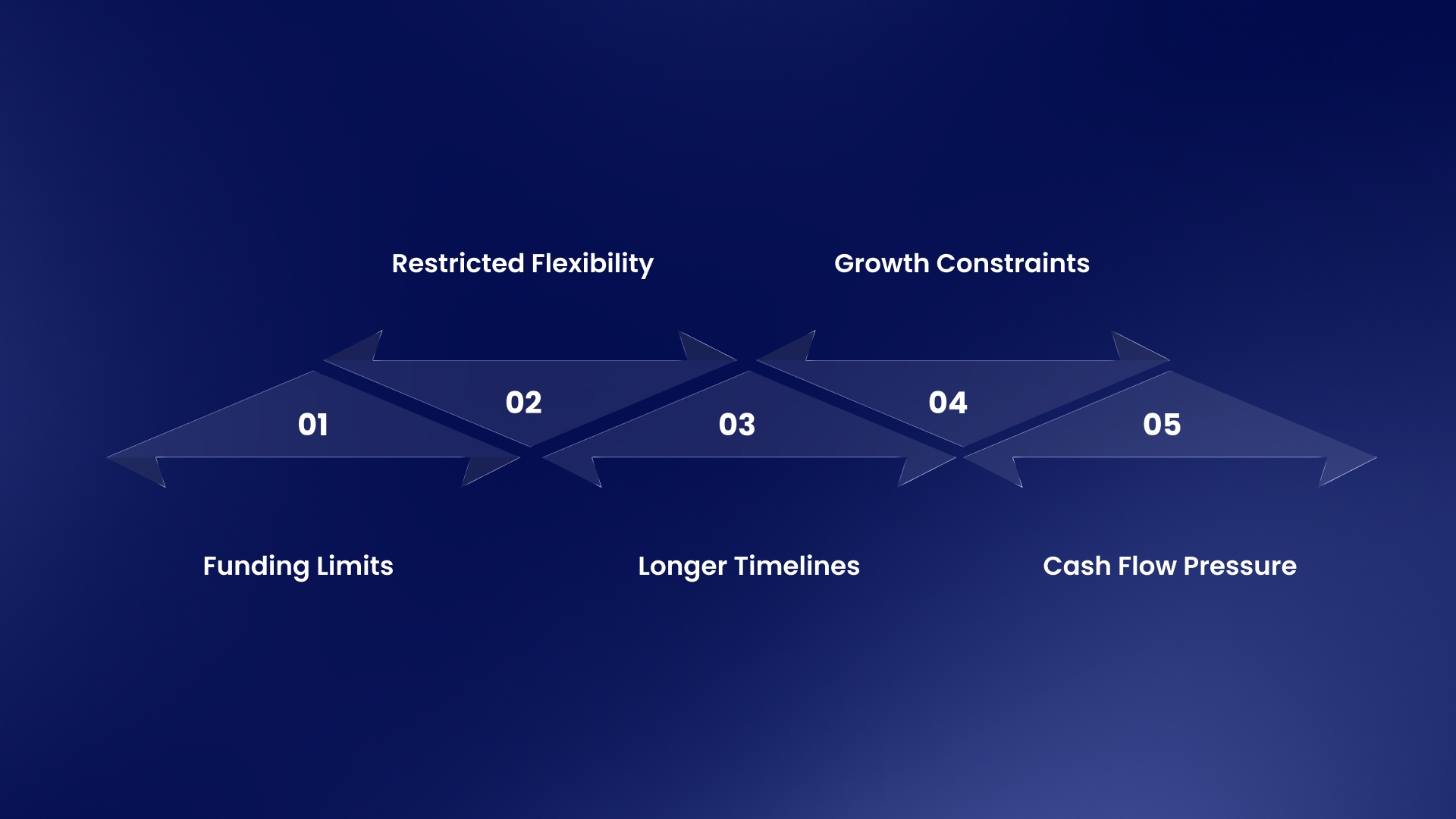

Mudra loans can help businesses access formal credit during the early stages of growth, but financing needs often become more complex as startups begin scaling operations.

Some of the common challenges growing startups face with Mudra loans include:

Funding Limits: Mudra loans may not be sufficient for startups managing aggressive expansion, higher operational costs, or rapid scaling plans.

Restricted Flexibility: Some businesses may require financing structures better aligned with fluctuating revenues or evolving cash flow cycles.

Longer Timelines: Approval and documentation processes can vary across lenders and may slow down time-sensitive business decisions.

Growth Constraints: Scaling startups often require recurring access to capital rather than one-time small-ticket financing.

Cash Flow Pressure: Fixed repayment structures may create pressure for businesses with seasonal demand or uneven revenue cycles.

Businesses exploring venture debt, revenue-based financing, or larger working capital solutions may need alternative funding models. Access to the right debt funding structure has become increasingly important for sustainable growth.

Recur Club connects startups with financing solutions designed around operational scale, cash flow needs, and expansion goals. You can access venture debt, working capital financing, invoice financing, and revenue-based funding through a network of 100+ lending partners.

For example, WeVOIS, an environmental services and SaaS company based in Jaipur, partnered with Recur Club to raise capital to expand operations and enter new markets. Through flexible debt financing and approvals within 48 hours, WeVOIS expanded into 6 new cities, increased revenue by 2.7x, and significantly improved EBITDA.

Funding Alternatives Beyond the Mudra Loan Scheme for Scaling Businesses

Scaling startups may require larger ticket sizes, recurring access to capital, faster approvals, or financing models better aligned with cash flow cycles and expansion plans.

Some commonly used funding alternatives include:

Revenue-Based Financing: Businesses repay funding through a percentage of future revenue, creating more flexibility during fluctuating growth cycles.

Venture Debt: Startups with strong growth potential or existing investor backing may use venture debt to extend runway without immediate equity dilution.

Working Capital Loans: These loans help businesses manage operational expenses, inventory cycles, payroll, and short-term cash flow gaps.

Invoice Financing: Businesses can unlock capital tied up in unpaid invoices to improve liquidity and maintain operational continuity.

AI-Led Debt Platforms: Modern debt marketplaces help startups access multiple lenders, faster underwriting, and customized financing structures through digital application processes.

The right financing structure depends on factors such as business stage, revenue stability, growth plans, and operational requirements. While Mudra loans can support smaller funding needs, scaling businesses often require more flexible and growth-oriented debt solutions.

Conclusion

While the Mudra Loan Scheme has improved access to formal credit, it may not suit every scaling business. Growing startups often need larger funding amounts, faster approvals, and more flexible financing structures as their operations expand.

Recur Club is an AI-native debt marketplace for startups and growing businesses, connecting them with institutional lenders across multiple debt categories. Its proprietary AI engine, AICA, helps lenders evaluate businesses faster through AI-driven underwriting, due diligence, and risk monitoring.

Looking for financing aligned with your growth plans? Connect with us to explore flexible funding options from institutional lenders to scale your business.

Frequently Asked Questions

1. What is the Mudra Loan Scheme?

The Mudra Loan Scheme, officially known as Pradhan Mantri Mudra Yojana, is a government-backed loan scheme that helps micro and small businesses access credit for income-generating activities.

2. Who is eligible for a Mudra loan?

Any Indian citizen with a business plan for a non-farm income-generating activity in manufacturing, trading, processing, or services can apply for a Mudra loan.

3. What is the maximum loan amount under the Mudra Loan Scheme?

Eligible borrowers can get loans of up to ₹20 lakh under the Mudra Loan Scheme.

4. What are the types of Mudra loans?

Mudra loans are offered under four categories: Shishu for loans up to ₹50,000, Kishore for loans above ₹50,000 and up to ₹5 lakh, Tarun for loans above ₹5 lakh and up to ₹10 lakh, and Tarun Plus for loans above ₹10 lakh and up to ₹20 lakh.

5. Can startups apply for Mudra loans?

Yes, startups and small businesses can apply if they are engaged in eligible income-generating activities and meet the lender’s requirements.

6. Is collateral required for a Mudra loan?

Generally, Mudra loans up to ₹20 lakh for micro and small enterprises are offered without collateral, subject to lender guidelines.

7. Where can I apply for a Mudra loan?

Borrowers can apply through banks, NBFCs, MFIs, and other eligible lending institutions. MUDRA itself does not lend directly to borrowers.

8. What documents are required for a Mudra loan?

The required documents depend on the lending institution, but applicants are usually asked for identity proof, address proof, business details, bank statements, and a business plan or loan application form.

9. What can a Mudra loan be used for?

A Mudra loan can be used for business expansion, working capital, equipment purchase, commercial vehicles, service businesses, trading activities, and other income-generating business needs.

10. What is the interest rate on Mudra loans?

Related Articles

Invoice Discounting vs Loans: Best Financing Option for Cash Flow Gaps

Compare invoice discounting and loans for business financing. Understand the pros, cons, and real-world applications to choose the right financing option.

A 2026 Guide to the Startup India Seed Fund Scheme: Application and Eligibility Criteria

Learn how the Startup India Seed Fund Scheme works in 2026, including eligibility criteria, application steps, funding limits, benefits, and considerations.

Solving Cash Flow Gaps: The Role of Working Capital Loans for Indian Startups in 2026

Explore when a loan for working capital is useful, its key uses, and how businesses can manage expenses and growth without cash flow gaps.

Talk to our experts and find the right financing solution.

Talk to Our Experts →