Invoice Discounting vs Loans: Best Financing Option for Cash Flow Gaps

Compare invoice discounting and loans for business financing. Understand the pros, cons, and real-world applications to choose the right financing option.

When cash isn’t in the bank, but invoices are due, the delay isn’t just annoying; it weakens your creditworthiness and limits access to finance. Research shows that firms experiencing frequent late payments face more restricted lending and less favorable loan terms, because lenders treat unpredictable cash flows as higher risk. In real terms, this means slower approvals, higher costs, and smaller credit lines for businesses trying to stay operational.

This blog breaks down the invoice discounting vs loan decision with the urgency it deserves: you’ll see how quickly each option delivers funds, what eligibility and documentation hurdles you’re likely to meet, and how repayment timing affects your cash cycle and planning. By comparing these practical criteria, you’ll be better positioned to choose the financing path that keeps your business liquid and agile, without equity loss or unnecessary risk.

Key Takeaways

Invoice discounting gives businesses quick access to working capital by turning unpaid invoices into cash, unlike traditional loans that take longer and have fixed repayment schedules.

Invoice discounting typically has fewer eligibility hurdles, as lenders mainly focus on the creditworthiness of the invoice and customer, not just business credit history.

Repayment in invoice discounting is tied to when customers pay their invoices, offering flexibility versus fixed EMIs of standard business loans.

Invoice discounting works best for short-term cash flow gaps, while traditional loans are more suited to long‑term investments or large capital needs.

Recur Club provides both funding through unpaid invoices and financing options by connecting businesses with its network of potential lenders, giving access to multiple capital sources and helping maintain predictable cash flow.

Invoice Discounting: A Quick and Flexible Financing Option for SMEs

As an SME owner, you’re no stranger to the challenges of managing cash flow. Late payments from clients can throw a wrench into your plans, delaying payments to suppliers, employees, or even funding the next growth initiative. But what if you could access cash tied up in unpaid invoices without waiting for your clients to settle up? That’s where invoice discounting comes in.

Invoice discounting is an innovative way for SMEs to unlock working capital quickly and without the burden of taking on more debt.

How Invoice Discounting Works for SMEs

Imagine your business has invoices that are due for payment, but you can’t wait weeks for customers to pay. Invoice discounting lets you access funds immediately against unpaid invoices. Here’s how it works:

You submit your unpaid invoices to a financing partner.

You get paid quickly, typically 70-90% of the invoice value.

Your customer pays the invoice in full.

You repay the financing partner, along with a small fee.

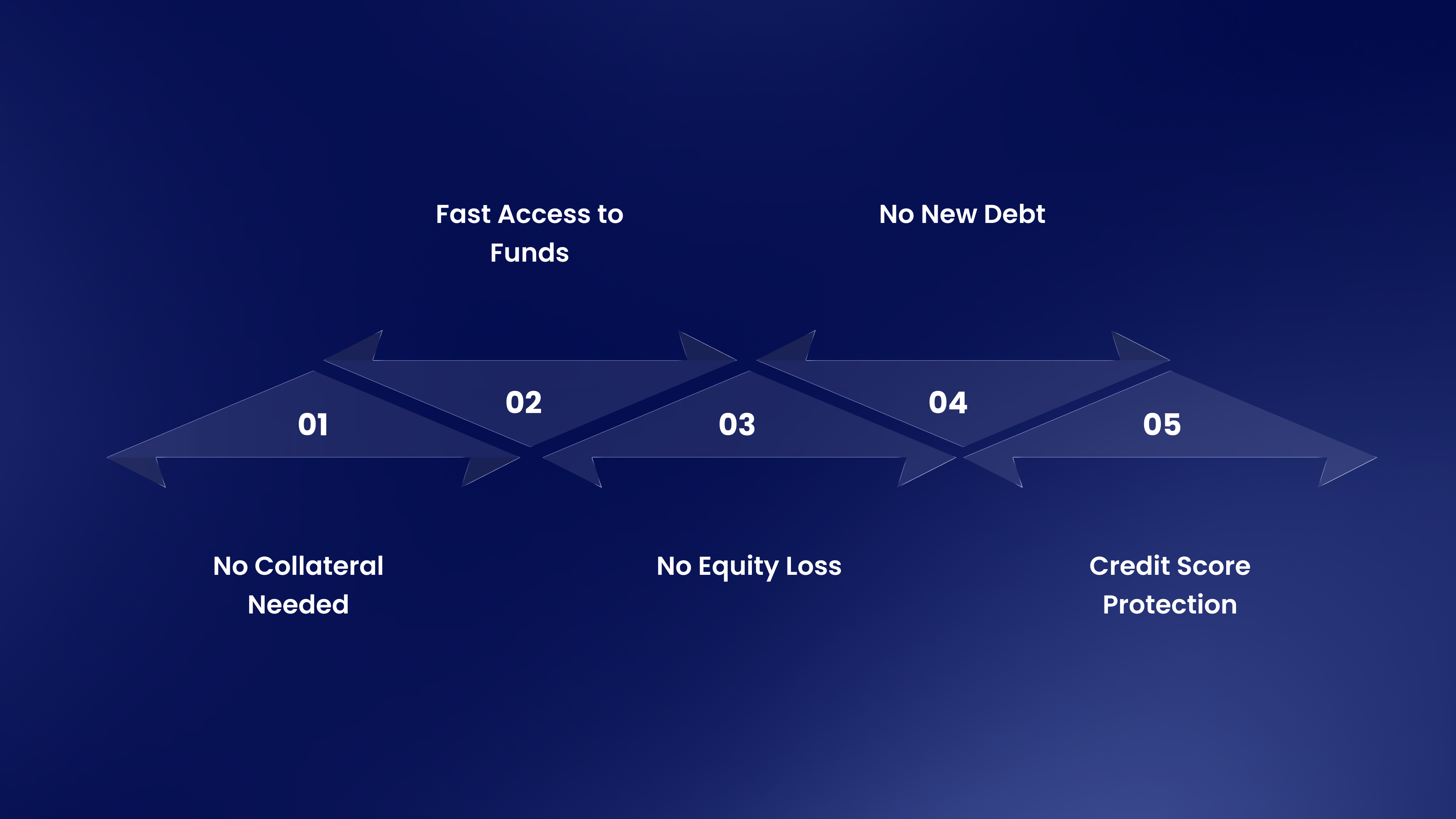

What Makes Invoice Discounting Unique?

1. No Collateral Needed

With invoice discounting, you don’t need to put up any assets as collateral. Your unpaid invoices are the only “security,” making it less risky for your business.

2. Fast Access to Funds

The process is quick and efficient, often allowing you to access funds in as little as 24-48 hours, perfect for businesses needing immediate capital to keep operations moving.

3. No Equity Loss

Unlike equity financing, you don’t need to give up any ownership or control of your business. Your business stays yours.

4. No New Debt

Invoice discounting isn’t a traditional loan; it’s a financing option based on your existing invoices. So, it doesn’t add more debt to your balance sheet.

5. Credit Score Protection

Since you aren’t borrowing money or using your assets, your credit score stays intact. Invoice discounting helps your business grow without affecting your future borrowing capacity.

Struggling with gaps between customer payments? Recur Club allows you to receive up to 90% advance on your outstanding invoices within 48 hours of submission, helping you bridge cash flow gaps of 30–90 days without adding debt or collateral.

Business Loans: Traditional Financing for Long-Term Goals

Business loans remain one of the most reliable and traditional sources of financing for SMEs. Whether you’re looking to purchase equipment, expand operations, or manage other major expenses, a business loan can provide the necessary capital.

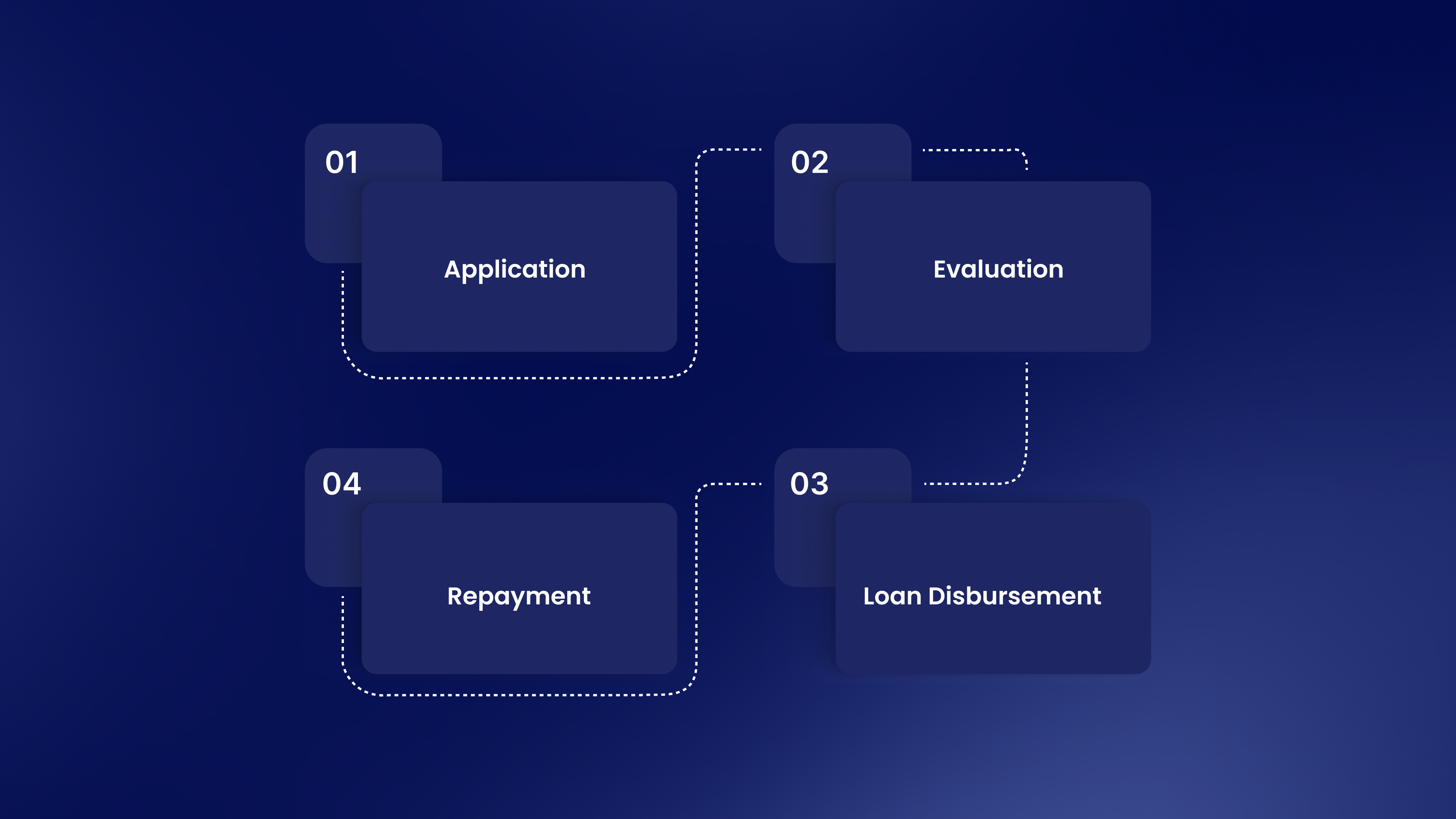

How Business Loans Work

Understanding the application process and how business loans function is the first step in securing financing for your business.

Step 1: Application – To apply for a business loan, you’ll typically need to provide essential documents, including financial statements, business plans, and tax returns. Lenders will use these to evaluate your eligibility.

Step 2: Evaluation – Lenders assess your creditworthiness, financial history, and business stability before offering loan terms.

Step 3: Loan Disbursement – Once approved, the loan amount is disbursed, typically as a lump sum, to cover business expenses.

Step 4: Repayment – You’ll repay the loan in fixed monthly instalments over an agreed term (usually 3–10 years).

When Business Loans Are Suitable for SMEs

Business loans are ideal for major, long-term investments that require substantial upfront capital. They work best in the following situations:

Business Expansion: Whether you’re adding a new location, launching a new product, or expanding into new markets, loans can provide the funding needed to support these growth initiatives.

Capital Expenditure: Purchasing large assets like machinery, equipment, or technology can be expensive. A business loan spreads out this cost over time, making it easier to manage.

Large, One-Time Expenses: If your business needs to finance a high-cost, long-term project, such as facility upgrades or new infrastructure, a loan is a suitable solution.

Key Factors and Risks

Before taking on a business loan, it's important to understand the loan terms, repayment schedules, and the risks involved. Here’s a simplified breakdown:

Interest Rates & Repayment Terms: Rates depend on your credit and the lender, and may be fixed or variable. Repayment typically lasts from 3 to 10 years, with monthly instalments.

Cash Flow Considerations: Monthly repayments can strain your cash flow, especially if your business faces seasonal fluctuations or lower revenue during some months.

Long-Term Commitment & Risks: Loans require long-term commitment, meaning you'll have consistent payments. Missing repayments can hurt your credit score and may even lead to penalties or business closure.

Suggested Read: Understanding Secured Loans: Types, Benefits, & How to Apply

Invoice Discounting vs Loan: Key Differences

The distinction between the two is not just about speed or paperwork. It goes deeper, into how the financing is structured, what it costs, and what it signals on your balance sheet.

Here is how they compare across the parameters that matter most for this decision.

Recur Club helps businesses access fast, flexible funding. Take Wellversed, a health & wellness startup in Gurgaon, for example. They raised ₹6.5 Crores+ in just 4 days, driving a 117% increase in revenue and a 63% boost in EBITDA.

Don’t let delays hold you back. Connect with lenders today and strengthen your business’s growth.

Suggested Read: Types of Loans and Advances: A Guide for SMEs

How to Choose Between Invoice Discounting and Business Loans: A Decision Framework

Choosing between invoice discounting and a business loan depends on your immediate needs and long-term goals. This framework will help you assess which option aligns with your business's financial situation.

Start by asking yourself a few key questions:

Do you need quick access to cash?

If you’re facing short-term cash flow issues, such as waiting for client payments to come through, invoice discounting might be a better option.Are you making a large, long-term investment?

If you’re planning to invest in business expansion, purchase equipment, or fund other large capital expenditures, a business loan may be more suitable.What’s your long-term strategy?

If you’re looking for a solution that allows you to retain control and manage your business without worrying about monthly repayments, invoice discounting offers more flexibility. But if you need substantial capital with predictable repayments over time, business loans are ideal.

Suggested Read: Loan-to-Value (LTV) Ratio: Meaning, Formula, and How to Calculate It

What Lenders Actually Evaluate Before Approving Either Option

The evaluation criteria differ meaningfully between the two instruments. This is part of why startups with limited credit history or no collateral often find invoice discounting more accessible than a working capital loan at the same business stage.

For invoice discounting, lenders primarily look at:

The creditworthiness of your buyer, not just yours. An invoice issued to a large corporate entity is far easier to discount than one issued to a smaller buyer with no credit history.

Invoice validity: clean, undisputed, with clear payment terms and no record of buyer disputes or short payments.

GST filing history provides lenders with a government-validated revenue trail, reducing underwriting uncertainty.

Business vintage of at least 10 to 12 months with consistent invoicing activity.

For a business loan, lenders evaluate:

6 to 12 months of bank statements: regular credits, minimal bounces, and consistent outflows that signal operational stability.

Revenue consistency and business vintage, most banks require a minimum of 2 years of operations.

Existing debt obligations and headroom for new repayments without creating cash flow stress.

Collateral availability is above certain thresholds, depending on the lender and facility size.

Equity backing or institutional investors in your cap table, which can sometimes unlock collateral-free options.

Suggested Read: Top 8 Invoice Discounting Platforms in India (2026)

One Risk With Each That Founders Often Overlook

Both instruments carry trade-offs that are worth understanding before you commit to a structure. The risk is rarely the instrument itself - it is using the wrong one for the wrong purpose.

With Invoice Discounting

The financing is only as strong as your invoice pipeline. If billing slows, between projects, between quarters, or after a large client pauses orders, the facility shrinks with it. Additionally, if a buyer disputes or delays payment on a discounted invoice, you may be required to return the advance, creating a liquidity problem at exactly the wrong moment.

With a Business Loan

The fixed EMI continues regardless of whether your customers have paid. In a slow receivables month, loan repayments drain the same cash pool that should cover operations. Over-reliance on debt without improving receivables management can mask the root cause rather than resolve it.

The right approach is to match the instrument to the actual cause and duration of the gap. Short-term receivable delays require short-term, receivables-backed financing, while structural or investment-linked capital needs require structured debt with appropriate tenures.

Suggested Read: Top 10 Short-Term Sources of Finance to Manage Your Business Cash Flow

How Recur Club Helps You Choose and Access the Right Instrument

The gap between knowing which instrument is right and actually accessing it at the right time is where most founders lose the most time. Multiple lender conversations, inconsistent offers, opaque pricing, and repeated documentation requests are the norm in the traditional debt market.

Recur Club is an AI-native debt marketplace for startups and growth-stage businesses in India. It has funded over Rs 3,000 crore across 2,000+ companies, with a network of 150+ institutional lenders, including Tata Capital, HSBC, and Aditya Birla Capital - across both invoice financing and working capital products.

What this means in practice:

You do not choose a product until you see your options. Recur Club’s platform connects with your financial data, evaluates your profile, and surfaces tailored offers across instruments - so you are comparing real terms, not brochure rates.

Every approved company is assigned a capital expert who maps the right debt structure to your business stage, lender mix, and cash flow cycle.

If you are sitting on outstanding invoices or planning your next capital raise, the better question is not “invoice discounting or loan” - it is what the right debt structure looks like for your specific business right now.

Suggested Read: Loans or Advances? Finding the Right Fit for Your Growth Stage

Conclusion

Invoice discounting offers faster, more flexible funding for short-term cash flow needs, while loans are better for long-term investments. For businesses seeking quick cash flow solutions, Recur Club connects you with lenders and provides funding through unpaid invoices.

Need fast funding? Visit Recur Club to get started today!

FAQs

1. What is the difference between invoice discounting and a loan?

Invoice discounting gives a business early access to funds tied up in unpaid customer invoices. A loan, on the other hand, is borrowed capital that must be repaid with interest over a fixed period. Invoice discounting is usually linked to receivables, while loans are linked to creditworthiness, repayment capacity, and sometimes collateral.

2. Is invoice discounting a type of loan?

Invoice discounting is not a traditional loan. It is a receivables-based financing method in which a business receives an advance against approved unpaid invoices. The repayment usually happens when the customer clears the invoice, unlike a loan, where the borrower pays fixed EMIs.

3. Which is better: invoice discounting or a business loan?

Invoice discounting is better for short-term cash flow gaps caused by delayed customer payments. A business loan is better when you need a larger lump sum for expansion, equipment purchase, marketing, or long-term business needs. The right choice depends on why you need funds and how quickly you can repay them.

4. Which option gives faster access to funds?

Invoice discounting is usually faster because the funding is based on verified invoices. Some providers mention disbursal within 24–72 hours or a few days after invoice approval. Business loans often take longer because lenders may check business vintage, credit history, documents, collateral, and repayment capacity.

5. Does invoice discounting require collateral?

Usually, invoice discounting does not require separate physical collateral, as the unpaid invoice serves as security for the financier. Business loans may or may not require collateral, depending on whether the loan is secured or unsecured and on the lender’s eligibility criteria.

6. How is repayment different in invoice discounting and loans?

In invoice discounting, repayment is linked to the customer’s invoice payment. Once the customer pays, the financier deducts charges and releases the balance. In a loan, the borrower repays through fixed EMIs or scheduled installments, regardless of whether the customer has paid on time.

7. Which is cheaper: invoice discounting or a loan?

The cost depends on the amount, tenure, lender, invoice quality, and business profile. Loans usually charge interest on the borrowed amount for the loan term. Invoice discounting charges fees on the invoice amount or the amount used, which can be cost-effective for short-term working capital, but should be compared carefully.

8. Can startups or small businesses use invoice discounting?

Yes, many small businesses use invoice discounting when they have unpaid invoices from reliable customers. It can be easier to access than a traditional loan because the financier often considers invoice quality and customer creditworthiness, not only the borrower’s long credit history.

9. Will customers know if I use invoice discounting?

It depends on the type of invoice discounting. In confidential invoice discounting, customers may not know that the invoice has been financed. In disclosed arrangements, customers may be aware that a third party is involved in the payment process.

10. When should a business choose invoice discounting over a loan?

A business should consider invoice discounting when it has unpaid invoices, needs quick working capital, wants to avoid fixed EMIs, and does not want to pledge additional collateral. A loan may be more suitable when the business needs a larger amount for long-term growth or to purchase assets.

Related Articles

What Is the Mudra Loan Scheme? Benefits, Eligibility & How to Apply in 2026

Learn what the Mudra Loan Scheme is, its benefits, eligibility criteria, loan categories, required documents, and how Indian businesses can apply for funding.

A 2026 Guide to the Startup India Seed Fund Scheme: Application and Eligibility Criteria

Learn how the Startup India Seed Fund Scheme works in 2026, including eligibility criteria, application steps, funding limits, benefits, and considerations.

Solving Cash Flow Gaps: The Role of Working Capital Loans for Indian Startups in 2026

Explore when a loan for working capital is useful, its key uses, and how businesses can manage expenses and growth without cash flow gaps.

Talk to our experts and find the right financing solution.

Talk to Our Experts →