SME Financing Through NBFCs in India: A Founder’s Guide

Why do MSMEs rely on NBFCs instead of banks? Learn how SME financing in India really works and how founders structure smarter debt.

For most SMEs in India, financing is not a one-time event. It is an ongoing operating decision that directly affects cash flow stability, growth speed, and survival during downturns.

Despite policy focus on SME lending, access to formal credit remains uneven. The issue is not the availability of lenders, but the design of credit systems. Indian SMEs operate with high variability in revenue, limited asset backing, and working capital cycles that do not align neatly with traditional lending models.

NBFCs have emerged as a critical layer in this system because they solve specific structural gaps rather than offering generic loans. Understanding their role requires looking at SME credit from the lender’s perspective, not just the borrower’s.

Key Takeaways

Use NBFC financing as an operating lever, not a last resort: It is best suited for managing cash-flow timing gaps in working capital and receivables.

Select lenders by purpose, not just pricing: Banks and NBFCs solve different problems, and the wrong match increases repayment and rollover risk.

Structure matters more than speed: Fast approvals lose value if short tenures or frequent EMIs strain long-term cash flows.

Financing must evolve as revenue stabilises: Standard NBFC loans rarely scale with growth; predictable cash flows need more flexible structures.

Structured, non-dilutive debt preserves ownership at scale: Thoughtful debt design supports growth without forcing early equity dilution.

SME Credit Gap in India: Where Bank Lending Breaks Down in Practice

Banks are built to manage risk at scale. Their lending frameworks prioritise predictability, collateral coverage, and standardisation. This creates friction when lending to SMEs, whose risk profiles are heterogeneous and dynamic.

From a bank’s perspective, the challenge is not SME intent but repayment visibility. Cash flows may be healthy over a year but uneven month to month. Receivables may be reliable but delayed. Asset ownership may be limited even when business viability is strong.

Why Bank Credit Models Exclude Viable SMEs

Bank underwriting depends on three pillars:

Historical financial statements

Fixed collateral coverage

Uniform credit scoring thresholds

These inputs reduce uncertainty but fail to capture real-time operating performance. SMEs that are profitable but asset-light, or growing faster than their financial history reflects, are often screened out early.

Approval timelines compound the issue. When credit decisions take weeks, they lose relevance for working capital-driven businesses.

Which SMEs Face the Highest Friction

Credit constraints are most acute for:

Businesses with high receivables exposure

Service and trading SMEs with limited fixed assets

Enterprises operating outside metro credit hubs

First-time formal borrowers

These segments form a large share of India’s SME base.

What Is an NBFC and Why NBFCs Are Structurally Suited for SME Lending

NBFCs occupy a different position in the financial system. They are regulated by the Reserve Bank of India but operate with greater balance sheet flexibility than banks.

Unlike banks, many NBFCs are purpose-built around:

Specific borrower profiles

Defined ticket sizes

Narrow industry or asset focus

This specialisation allows NBFCs to price risk rather than avoid it.

How NBFC Underwriting Actually Works for SMEs

NBFCs prioritise current operating data over long-term asset ownership. Credit assessment typically focuses on:

Bank account cash flow trends

GST filings and turnover consistency

Receivables quality and concentration

Sector-specific operating benchmarks

Instead of asking whether a business fits a predefined template, NBFCs ask whether cash flows can service debt under realistic scenarios. This shift in underwriting philosophy is central to their role in SME financing.

Why NBFCs Are Critical to SME Financing in India

NBFCs are not simply faster lenders. Their importance lies in how they align credit structures with SME economics.

Speed That Matches Business Decision Cycles

SME financing decisions are often triggered by operational events such as inventory build-up, vendor negotiations, or receivables delays. NBFCs design credit processes around these timelines rather than annual planning cycles.

Risk Pricing Instead of Risk Avoidance

NBFCs accept higher variability in borrower profiles and compensate through pricing, structuring, and monitoring. This enables credit access where banks remain constrained by uniform thresholds.

Localised Credit Judgement

Many NBFCs rely on regional presence and contextual understanding. This allows credit decisions based on business behaviour rather than documentation alone, particularly in non-metro markets.

Also read: Decoding the Loan Components in Working Capital Finance

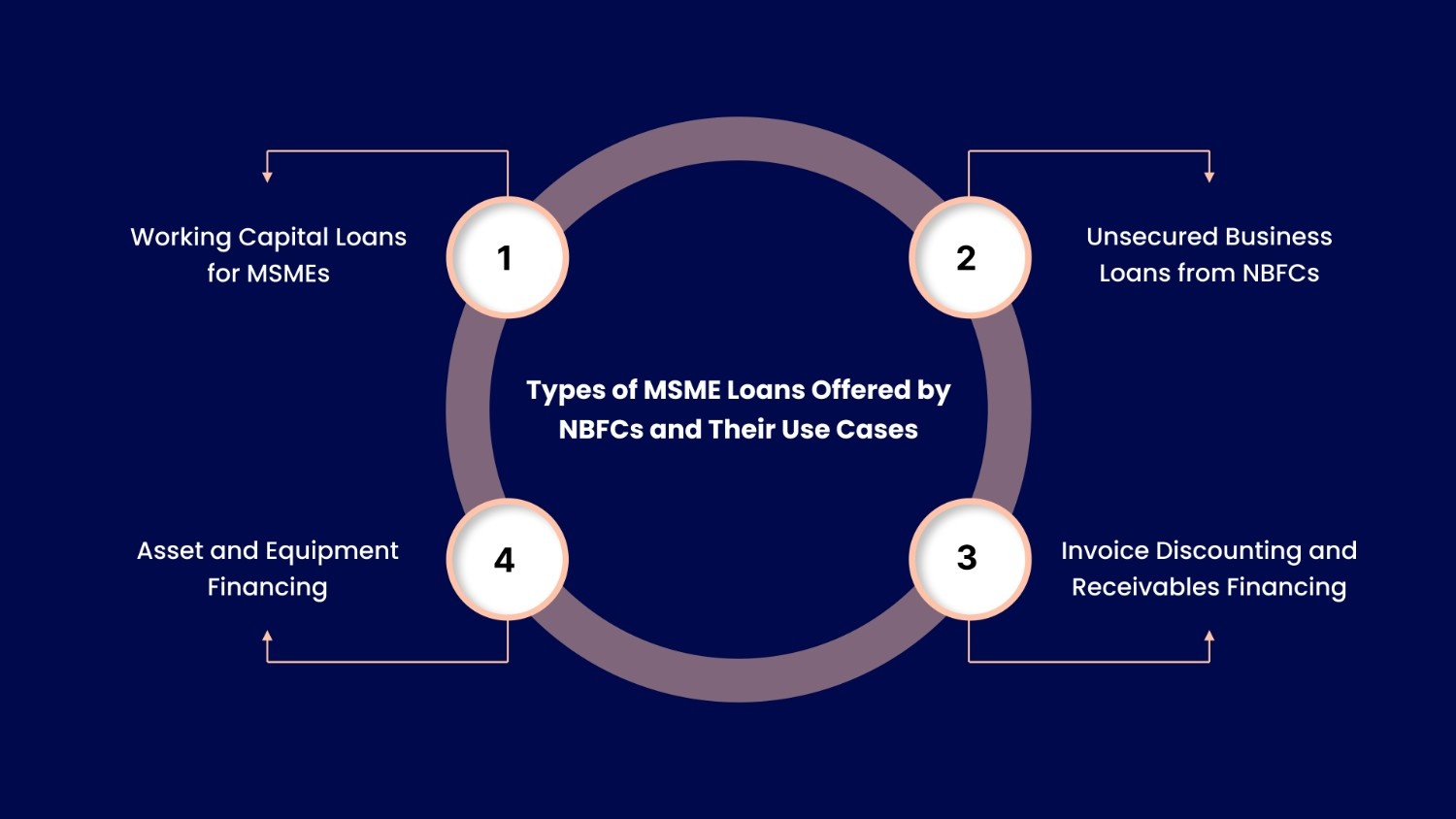

Types of SME Loans Offered by NBFCs and Their Use Cases

NBFC loan products are differentiated by how SMEs use capital, not by generic categories.

Working Capital Loans for SMEs

Used to fund the day-to-day operating cycle rather than long-term expansion. These loans typically bridge timing gaps between inventory procurement, vendor payments, payroll, and receivables realisation. NBFCs structure repayments around expected cash inflows, making this product suitable for businesses with predictable operating cycles but uneven liquidity timing.

Unsecured Business Loans from NBFCs

Designed for asset-light businesses where value is generated through operations rather than fixed assets. NBFCs underwrite these loans based on cash flow visibility, revenue stability, and customer quality. Pricing reflects operating risk rather than asset coverage, which allows access to credit without collateral but at a higher cost.

Invoice Discounting and Receivables Financing

Enables SMEs to convert confirmed invoices into immediate working capital. NBFCs advance funds against receivables, reducing dependence on customer payment timelines. This is particularly relevant for businesses supplying to larger corporations or government entities with longer credit periods.

Asset and Equipment Financing for Small Businesses

Used when assets directly contribute to revenue generation, such as machinery, commercial vehicles, or production equipment. NBFCs align repayment schedules with the income generated by the asset, making this form of financing suitable for manufacturing, logistics, and trade-led SMEs.

NBFC vs Bank Loans for SMEs: How Founders and CFOs Decide

The choice between bank loans and NBFC financing is a capital structure decision rather than a preference for one lender type.

In practice, the decision is driven by use case, timing, and balance sheet constraints.

Bank loans

Better suited for long-tenure borrowing backed by fixed assets. Banks typically offer lower cost of capital but require stronger collateral coverage, longer operating histories, and standardised underwriting.

NBFC loans

Better suited for short- to medium-tenure borrowing linked to operating cash flows. NBFCs prioritise speed, flexibility, and cash flow visibility, making them relevant when timing and adaptability matter more than pricing.

Most mature SMEs use a combination of both, relying on banks for stable, long-term funding and NBFCs for working capital and operational flexibility.

Also Read: A Complete Guide to How Small Business Loans Work in India

Risks of NBFC Financing from an SME Perspective

NBFC financing improves access to credit, but it also introduces specific risks that SMEs need to evaluate carefully.

Borrowing costs are typically higher than bank loans because NBFCs face higher funding costs and greater exposure to cash flow volatility.

The primary risk for SMEs is misalignment, using short-tenure or high-frequency repayment loans to fund long-term or uncertain needs.

During economic slowdowns, overestimated cash flow stability can quickly translate into repayment stress.

For SMEs, loan structure, tenure, and repayment design are often more important than headline interest rates.

When SMEs Outgrow Standard NBFC Loans

As SMEs scale, plain working capital loans can become restrictive rather than enabling.

Businesses with improving margins and predictable revenues often need capital that:

Adjusts as the business grows

Preserves ownership and control

Avoids rigid, front-loaded repayment schedules

At this stage, platforms such as Recur Club help founders navigate more complex debt structures by combining capital advisory with access to institutional lenders. This shift is commonly seen among SMEs that begin with short-term NBFC working capital and later require more flexible structures as revenues stabilise. In practice, businesses in sectors such as SaaS, D2C, and manufacturing often reach this point once growth outpaces the rigidity of plain working capital loans.

How Structured, Non-Dilutive Capital Complements NBFC Financing

Structured capital sits between traditional loans and equity. It is typically used by SMEs that have outgrown plain working capital loans but are not yet ready to dilute ownership.

Unlike standard NBFC loans, structured capital aligns repayment obligations more closely with business performance. This reduces cash flow strain during growth phases while still providing access to institutional debt.

Capital advisory platforms help SMEs:

Compare funding options across multiple institutional lenders

Structure repayment terms around operating cash flows rather than fixed schedules

Optimise trade-offs between cost of capital, flexibility, and control

Recur Club operates in this layer by helping businesses access structured, non-dilutive capital through solutions aligned to different stages of growth. Recur Swift is typically used for early-stage and operational funding needs where speed and flexibility matter, while Recur Scale supports growth-stage SMEs seeking larger, more structured capital without equity dilution. Both are designed to complement NBFC financing rather than replace it.

Conclusion

Access to capital is no longer the primary constraint for SMEs. The real challenge is choosing financing structures that remain resilient as the business grows and operating conditions change.

NBFCs have expanded the range of credit options available to SMEs, but sustainable growth depends on how that credit is structured, timed, and combined with other forms of non-dilutive capital. Founders and finance leaders who treat financing as an operating decision, rather than a one-time transaction, are better positioned to manage risk and scale efficiently.

If you are evaluating funding options or planning your next phase of growth, connect with Recur Club to explore debt structures aligned with your business model. You can speak with a capital expert to understand what type of non-dilutive financing makes sense for your stage.

FAQs

Q: What is SME financing through NBFCs in India?

A: SME financing through NBFCs refers to loans provided by non-bank lenders that focus on cash flow–based underwriting rather than heavy collateral. These loans are commonly used for working capital, receivables, and short-term operational needs.

Q: Why do SMEs choose NBFC loans instead of bank loans?

A: SMEs choose NBFC loans because approvals are faster and repayment structures are more flexible. NBFCs are better suited for businesses with uneven cash flows or limited fixed assets.

Q: What types of SME loans do NBFCs offer in India?

A: NBFCs offer working capital loans, unsecured business loans, invoice discounting, and asset or equipment financing. These products are structured around how SMEs actually use capital.

Q: Are NBFC loans more expensive than bank loans for SMEs?

A: Yes, NBFC loans usually carry higher interest rates due to higher funding costs and cash flow risk. The trade-off is faster access and greater flexibility compared to banks.

Q: How do NBFCs assess SME loan eligibility?

A: NBFCs evaluate eligibility using bank statement cash flows, GST data, receivables quality, and sector benchmarks. Collateral is considered but is not the primary driver.

Related Articles

Short Term Debt on the Balance Sheet: Explained Simply (2026)

Learn how short term debt appears on the balance sheet, with clear examples, classification rules, and reporting tips for startup finance teams.

CGTMSE Maximum Coverage: Eligibility, Limits, and Loan Structure in 2026

Understand CGTMSE maximum coverage, including eligibility criteria, guarantee limits, loan structure, and how MSMEs can access collateral-free business loans.

What Is Capital Growth, and How Can Startups Use Debt to Drive It?

Learn what capital growth is and how it impacts SMEs, business expansion, and debt strategies, with actionable insights for Indian entrepreneurs.

Talk to our experts and find the right financing solution.

Talk to Our Experts →